Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Portland General Electric Company (NYSE:POR) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Portland General Electric’s Net Debt?

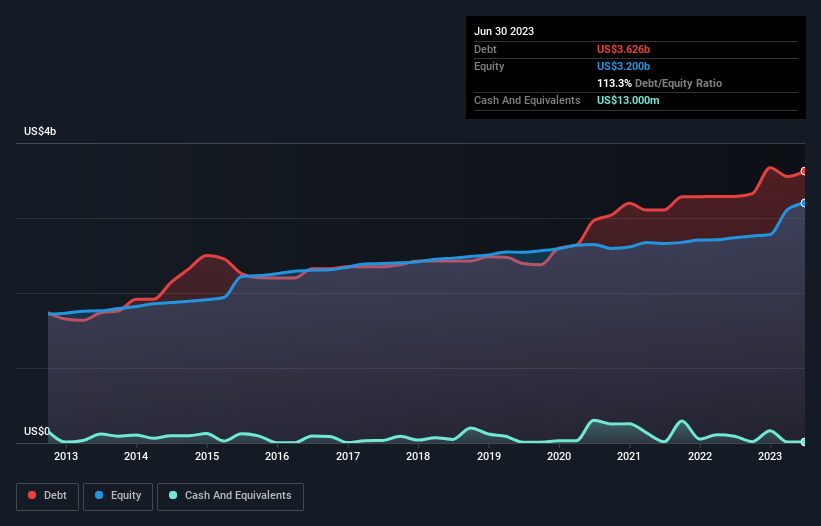

The image below, which you can click on for greater detail, shows that at June 2023 Portland General Electric had debt of US$3.63b, up from US$3.29b in one year. Net debt is about the same, since the it doesn’t have much cash.

A Look At Portland General Electric’s Liabilities

According to the last reported balance sheet, Portland General Electric had liabilities of US$761.0m due within 12 months, and liabilities of US$6.41b due beyond 12 months. Offsetting this, it had US$13.0m in cash and US$310.0m in receivables that were due within 12 months. So its liabilities total US$6.85b more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$4.43b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Portland General Electric would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Portland General Electric’s debt to EBITDA ratio (4.5) suggests that it uses some debt, its interest cover is very weak, at 2.2, suggesting high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Even more troubling is the fact that Portland General Electric actually let its EBIT decrease by 4.7% over the last year. If that earnings trend continues the company will face an uphill battle to pay off its debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Portland General Electric’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Portland General Electric saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Portland General Electric’s level of total liabilities and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. And furthermore, its net debt to EBITDA also fails to instill confidence. It’s also worth noting that Portland General Electric is in the Electric Utilities industry, which is often considered to be quite defensive. Taking into account all the aforementioned factors, it looks like Portland General Electric has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. There’s no doubt that we learn most about debt from the balance sheet.