Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Graham Holdings Company (NYSE:GHC) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Graham Holdings’s Debt?

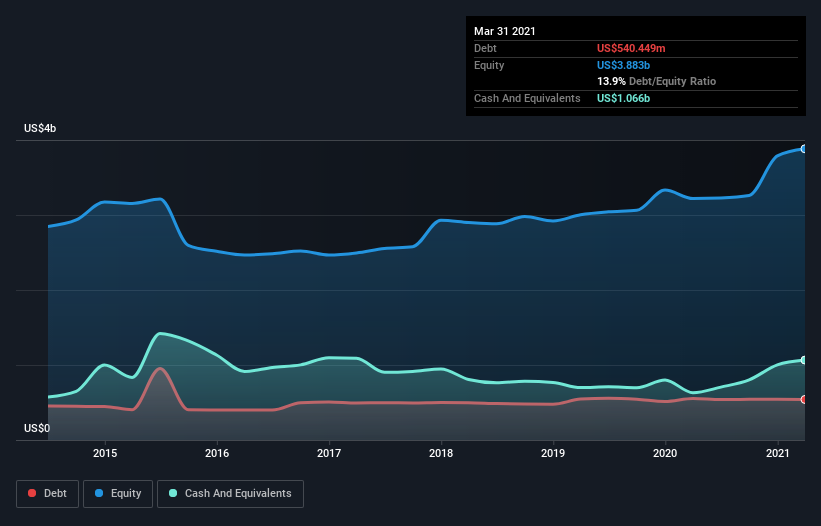

The chart below, which you can click on for greater detail, shows that Graham Holdings had US$540.4m in debt in March 2021; about the same as the year before. But it also has US$1.07b in cash to offset that, meaning it has US$525.3m net cash.

A Look At Graham Holdings’ Liabilities

We can see from the most recent balance sheet that Graham Holdings had liabilities of US$927.7m falling due within a year, and liabilities of US$1.71b due beyond that. Offsetting these obligations, it had cash of US$1.07b as well as receivables valued at US$530.6m due within 12 months. So it has liabilities totalling US$1.04b more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Graham Holdings is worth US$3.28b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution. While it does have liabilities worth noting, Graham Holdings also has more cash than debt, so we’re pretty confident it can manage its debt safely.

In fact Graham Holdings’s saving grace is its low debt levels, because its EBIT has tanked 25% in the last twelve months. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Graham Holdings’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While Graham Holdings has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last three years, Graham Holdings’s free cash flow amounted to 46% of its EBIT, less than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

Although Graham Holdings’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$525.3m. So although we see some areas for improvement, we’re not too worried about Graham Holdings’s balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.