Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Genuine Parts Company (NYSE:GPC) makes use of debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Genuine Parts’s Debt?

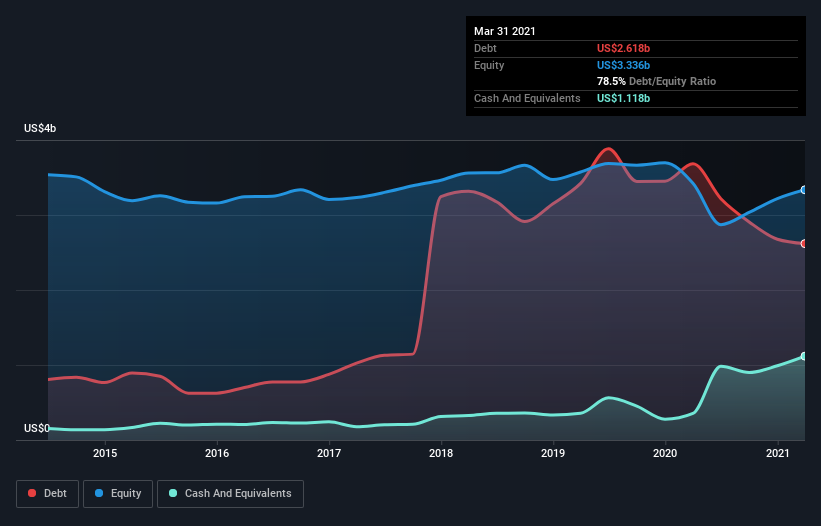

The image below, which you can click on for greater detail, shows that Genuine Parts had debt of US$2.35b at the end of March 2021, a reduction from US$3.68b over a year. However, it does have US$1.12b in cash offsetting this, leading to net debt of about US$1.23b.

How Strong Is Genuine Parts’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Genuine Parts had liabilities of US$6.34b due within 12 months and liabilities of US$4.27b due beyond that. On the other hand, it had cash of US$1.12b and US$1.81b worth of receivables due within a year. So it has liabilities totalling US$7.68b more than its cash and near-term receivables, combined.

Genuine Parts has a very large market capitalization of US$18.0b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Genuine Parts’s net debt is only 0.89 times its EBITDA. And its EBIT easily covers its interest expense, being 12.3 times the size. So we’re pretty relaxed about its super-conservative use of debt. The good news is that Genuine Parts has increased its EBIT by 7.8% over twelve months, which should ease any concerns about debt repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Genuine Parts’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Happily for any shareholders, Genuine Parts actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

The good news is that Genuine Parts’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its conversion of EBIT to free cash flow is also very heartening. Taking all this data into account, it seems to us that Genuine Parts takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.