Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Evergy, Inc. (NASDAQ:EVRG) does have debt on its balance sheet. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Evergy’s Debt?

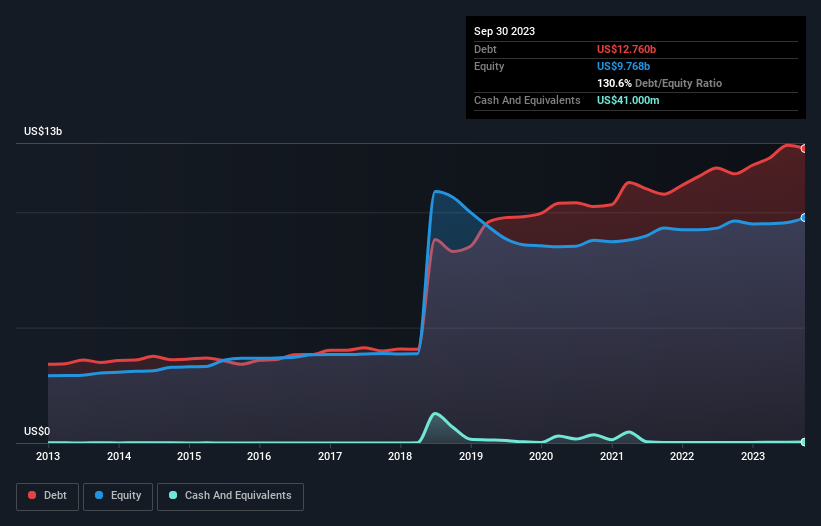

You can click the graphic below for the historical numbers, but it shows that as of September 2023 Evergy had US$12.8b of debt, an increase on US$11.7b, over one year. And it doesn’t have much cash, so its net debt is about the same.

A Look At Evergy’s Liabilities

According to the last reported balance sheet, Evergy had liabilities of US$4.81b due within 12 months, and liabilities of US$16.0b due beyond 12 months. On the other hand, it had cash of US$41.0m and US$345.0m worth of receivables due within a year. So it has liabilities totalling US$20.5b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the US$11.9b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Evergy would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Weak interest cover of 2.5 times and a disturbingly high net debt to EBITDA ratio of 5.6 hit our confidence in Evergy like a one-two punch to the gut. The debt burden here is substantial. More concerning, Evergy saw its EBIT drop by 5.9% in the last twelve months. If that earnings trend continues the company will face an uphill battle to pay off its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Evergy can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Evergy saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both Evergy’s conversion of EBIT to free cash flow and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. And even its interest cover fails to inspire much confidence. We should also note that Electric Utilities industry companies like Evergy commonly do use debt without problems. After considering the datapoints discussed, we think Evergy has too much debt. That sort of riskiness is ok for some, but it certainly doesn’t float our boat. The balance sheet is clearly the area to focus on when you are analysing debt.