The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Terex Corporation (NYSE:TEX) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Terex’s Debt?

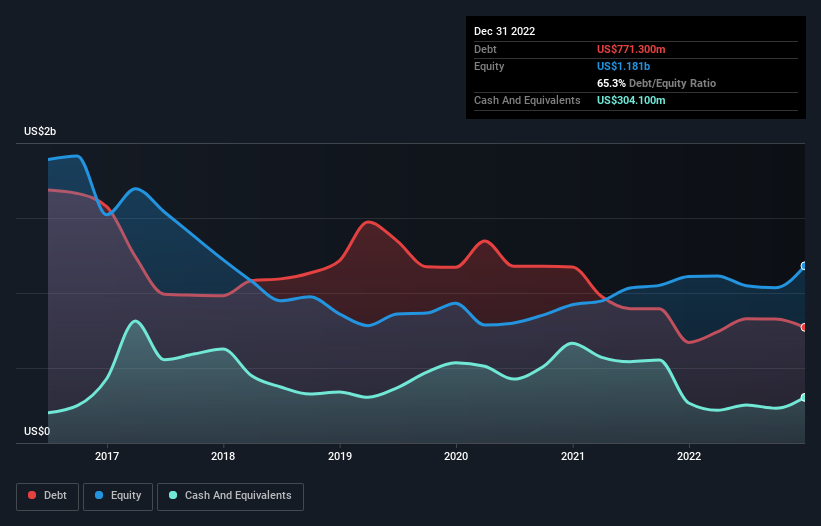

The image below, which you can click on for greater detail, shows that at December 2022 Terex had debt of US$771.3m, up from US$670.6m in one year. However, because it has a cash reserve of US$304.1m, its net debt is less, at about US$467.2m.

How Healthy Is Terex’s Balance Sheet?

We can see from the most recent balance sheet that Terex had liabilities of US$998.6m falling due within a year, and liabilities of US$938.3m due beyond that. Offsetting this, it had US$304.1m in cash and US$562.2m in receivables that were due within 12 months. So its liabilities total US$1.07b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Terex is worth US$3.09b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Terex has net debt of just 1.00 times EBITDA, indicating that it is certainly not a reckless borrower. And this view is supported by the solid interest coverage, with EBIT coming in at 9.1 times the interest expense over the last year. Also positive, Terex grew its EBIT by 26% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Terex can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Terex produced sturdy free cash flow equating to 66% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Terex’s EBIT growth rate suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! When we consider the range of factors above, it looks like Terex is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders.