Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Targa Resources Corp. (NYSE:TRGP) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Targa Resources Carry?

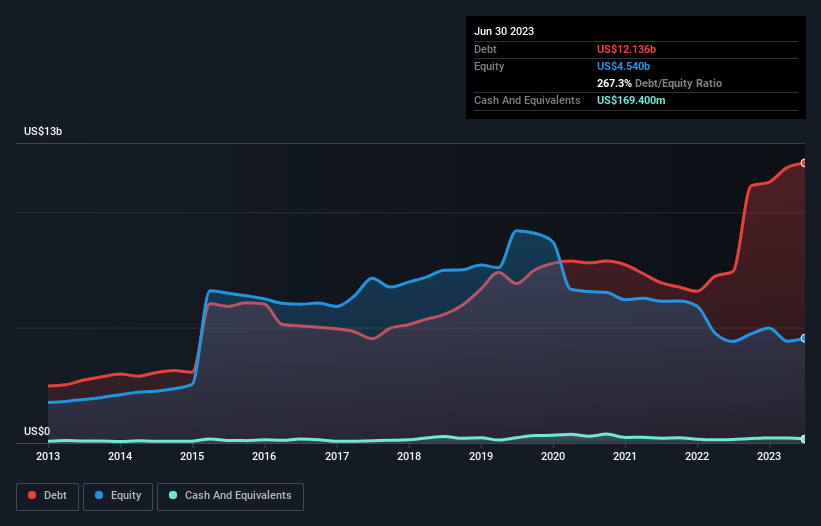

You can click the graphic below for the historical numbers, but it shows that as of June 2023 Targa Resources had US$12.1b of debt, an increase on US$7.43b, over one year. And it doesn’t have much cash, so its net debt is about the same.

A Look At Targa Resources’ Liabilities

We can see from the most recent balance sheet that Targa Resources had liabilities of US$2.32b falling due within a year, and liabilities of US$12.6b due beyond that. Offsetting this, it had US$169.4m in cash and US$988.1m in receivables that were due within 12 months. So its liabilities total US$13.8b more than the combination of its cash and short-term receivables.

This is a mountain of leverage even relative to its gargantuan market capitalization of US$19.4b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Targa Resources has a debt to EBITDA ratio of 3.2 and its EBIT covered its interest expense 4.1 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. The good news is that Targa Resources grew its EBIT a smooth 66% over the last twelve months. Like a mother’s loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Targa Resources can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Targa Resources generated free cash flow amounting to a very robust 82% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that Targa Resources’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. All these things considered, it appears that Targa Resources can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. The balance sheet is clearly the area to focus on when you are analysing debt.