Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Abeona Therapeutics Inc. (NASDAQ:ABEO) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Abeona Therapeutics Carry?

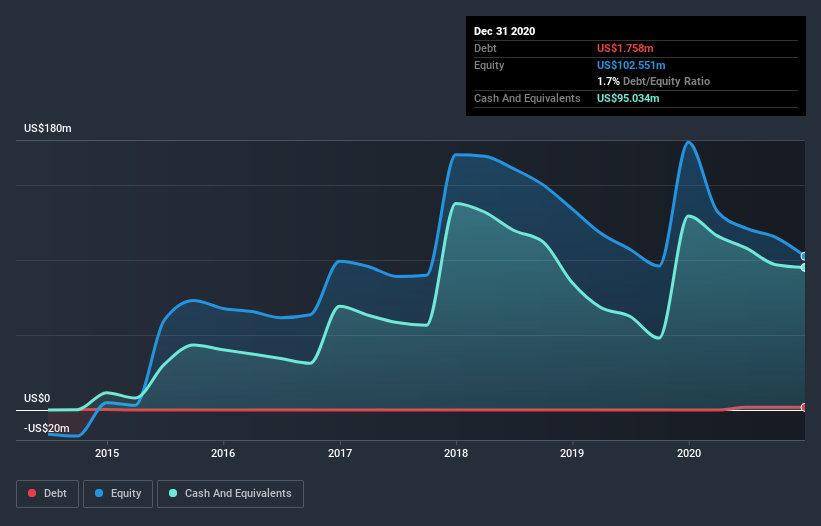

As you can see below, at the end of December 2020, Abeona Therapeutics had US$1.76m of debt, up from none a year ago. Click the image for more detail. However, its balance sheet shows it holds US$95.0m in cash, so it actually has US$93.3m net cash.

How Healthy Is Abeona Therapeutics’ Balance Sheet?

The latest balance sheet data shows that Abeona Therapeutics had liabilities of US$42.0m due within a year, and liabilities of US$6.69m falling due after that. Offsetting this, it had US$95.0m in cash and US$7.00m in receivables that were due within 12 months. So it actually has US$53.4m more liquid assets than total liabilities.

This surplus liquidity suggests that Abeona Therapeutics’ balance sheet could take a hit just as well as Homer Simpson’s head can take a punch. With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Succinctly put, Abeona Therapeutics boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Abeona Therapeutics can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Abeona Therapeutics managed to produce its first revenue as a listed company, but given the lack of profit, shareholders will no doubt be hoping to see some strong increases.

So How Risky Is Abeona Therapeutics?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Abeona Therapeutics lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$36m and booked a US$84m accounting loss. However, it has net cash of US$93.3m, so it has a bit of time before it will need more capital. The good news for shareholders is that Abeona Therapeutics has dazzling revenue growth, so there’s a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.