Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Reliance Steel & Aluminum Co. (NYSE:RS) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Reliance Steel & Aluminum’s Net Debt?

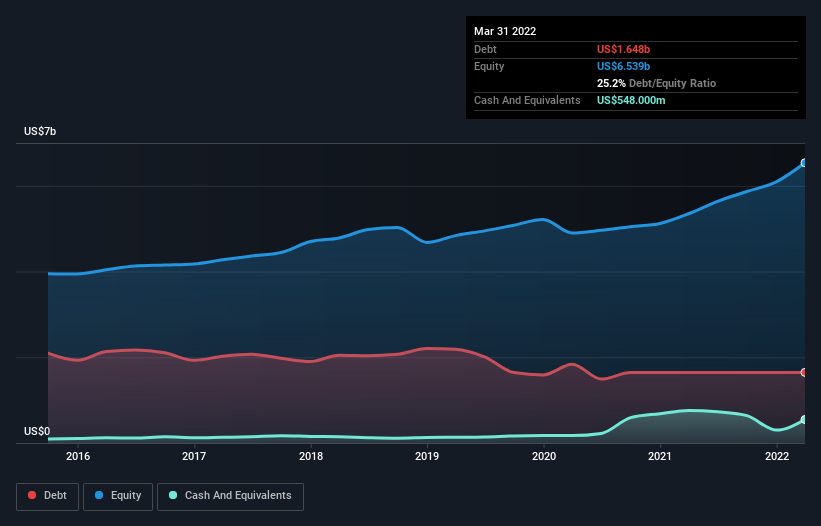

The chart below, which you can click on for greater detail, shows that Reliance Steel & Aluminum had US$1.65b in debt in March 2022; about the same as the year before. However, it does have US$548.0m in cash offsetting this, leading to net debt of about US$1.10b.

A Look At Reliance Steel & Aluminum’s Liabilities

The latest balance sheet data shows that Reliance Steel & Aluminum had liabilities of US$1.20b due within a year, and liabilities of US$2.38b falling due after that. Offsetting this, it had US$548.0m in cash and US$2.08b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$948.8m.

Given Reliance Steel & Aluminum has a humongous market capitalization of US$10.7b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Reliance Steel & Aluminum’s net debt is only 0.43 times its EBITDA. And its EBIT covers its interest expense a whopping 36.9 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Better yet, Reliance Steel & Aluminum grew its EBIT by 176% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Reliance Steel & Aluminum’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Reliance Steel & Aluminum recorded free cash flow worth 70% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

The good news is that Reliance Steel & Aluminum’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its EBIT growth rate is also very heartening. Overall, we don’t think Reliance Steel & Aluminum is taking any bad risks, as its debt load seems modest. So we’re not worried about the use of a little leverage on the balance sheet. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet.