Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Rambus Inc. (NASDAQ:RMBS) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

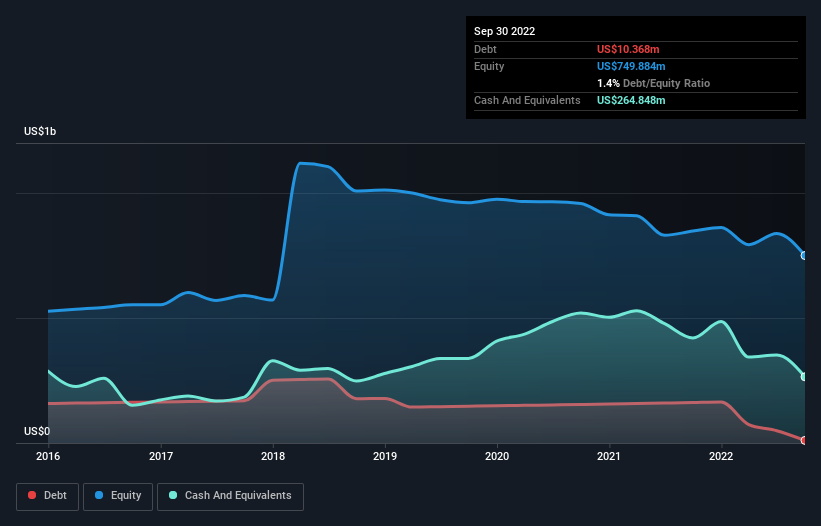

What Is Rambus’s Debt?

As you can see below, Rambus had US$10.4m of debt at September 2022, down from US$161.7m a year prior. But it also has US$264.8m in cash to offset that, meaning it has US$254.5m net cash.

How Healthy Is Rambus’ Balance Sheet?

The latest balance sheet data shows that Rambus had liabilities of US$116.4m due within a year, and liabilities of US$102.7m falling due after that. Offsetting this, it had US$264.8m in cash and US$180.6m in receivables that were due within 12 months. So it can boast US$226.3m more liquid assets than total liabilities.

This surplus suggests that Rambus has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Rambus boasts net cash, so it’s fair to say it does not have a heavy debt load!

Even more impressive was the fact that Rambus grew its EBIT by 871% over twelve months. That boost will make it even easier to pay down debt going forward. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Rambus can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Rambus has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, Rambus actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Rambus has net cash of US$254.5m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of US$229m, being 462% of its EBIT. So we don’t think Rambus’s use of debt is risky.