Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Ralph Lauren Corporation (NYSE:RL) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Ralph Lauren’s Net Debt?

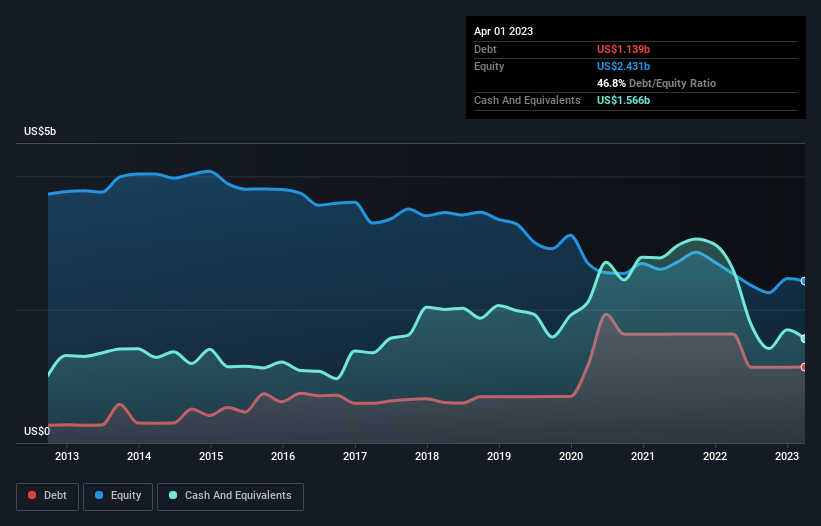

The image below, which you can click on for greater detail, shows that Ralph Lauren had debt of US$1.14b at the end of April 2023, a reduction from US$1.64b over a year. But it also has US$1.57b in cash to offset that, meaning it has US$427.2m net cash.

How Healthy Is Ralph Lauren’s Balance Sheet?

The latest balance sheet data shows that Ralph Lauren had liabilities of US$1.49b due within a year, and liabilities of US$2.87b falling due after that. On the other hand, it had cash of US$1.57b and US$579.7m worth of receivables due within a year. So its liabilities total US$2.21b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Ralph Lauren has a market capitalization of US$8.00b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, Ralph Lauren boasts net cash, so it’s fair to say it does not have a heavy debt load!

But the other side of the story is that Ralph Lauren saw its EBIT decline by 8.2% over the last year. That sort of decline, if sustained, will obviously make debt harder to handle. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Ralph Lauren’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Ralph Lauren may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, Ralph Lauren produced sturdy free cash flow equating to 58% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

Although Ralph Lauren’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of US$427.2m. So we are not troubled with Ralph Lauren’s debt use. There’s no doubt that we learn most about debt from the balance sheet.