Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Portland General Electric Company (NYSE:POR) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Portland General Electric’s Debt?

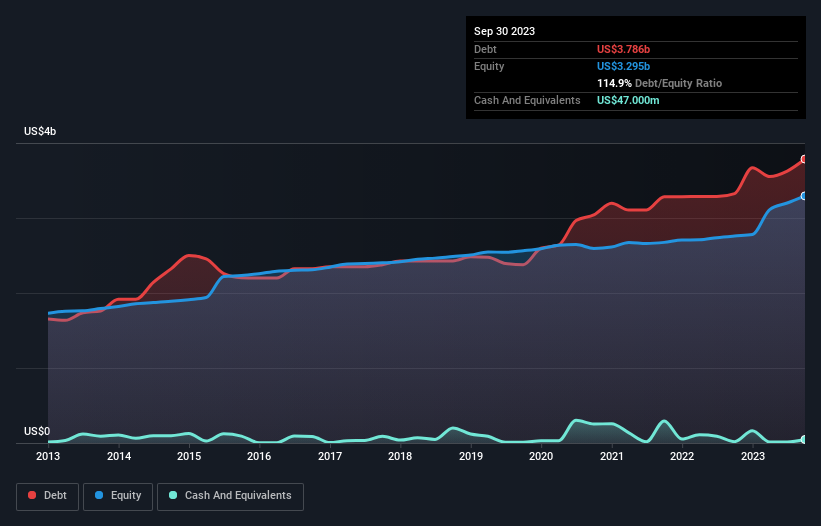

As you can see below, at the end of September 2023, Portland General Electric had US$3.79b of debt, up from US$3.33b a year ago. Click the image for more detail. Net debt is about the same, since the it doesn’t have much cash.

How Healthy Is Portland General Electric’s Balance Sheet?

The latest balance sheet data shows that Portland General Electric had liabilities of US$636.0m due within a year, and liabilities of US$6.67b falling due after that. Offsetting this, it had US$47.0m in cash and US$364.0m in receivables that were due within 12 months. So it has liabilities totalling US$6.90b more than its cash and near-term receivables, combined.

The deficiency here weighs heavily on the US$4.13b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. At the end of the day, Portland General Electric would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Portland General Electric’s debt to EBITDA ratio (4.6) suggests that it uses some debt, its interest cover is very weak, at 2.2, suggesting high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Even more troubling is the fact that Portland General Electric actually let its EBIT decrease by 5.8% over the last year. If that earnings trend continues the company will face an uphill battle to pay off its debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Portland General Electric’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Portland General Electric burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Portland General Electric’s conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. And even its net debt to EBITDA fails to inspire much confidence. We should also note that Electric Utilities industry companies like Portland General Electric commonly do use debt without problems. After considering the datapoints discussed, we think Portland General Electric has too much debt. While some investors love that sort of risky play, it’s certainly not our cup of tea. The balance sheet is clearly the area to focus on when you are analysing debt.