Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Overstock.com, Inc. (NASDAQ:OSTK) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Overstock.com’s Debt?

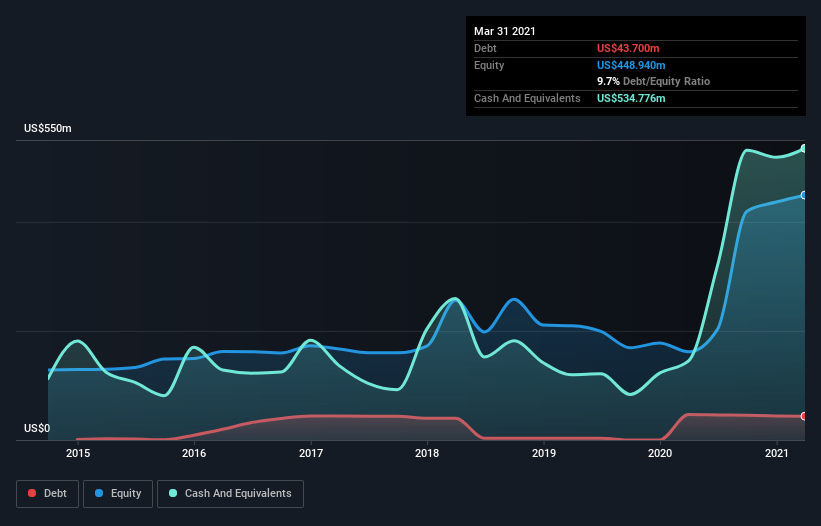

You can click the graphic below for the historical numbers, but it shows that Overstock.com had US$43.7m of debt in March 2021, down from US$46.8m, one year before. However, its balance sheet shows it holds US$534.8m in cash, so it actually has US$491.1m net cash.

How Strong Is Overstock.com’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Overstock.com had liabilities of US$370.0m due within 12 months and liabilities of US$74.8m due beyond that. Offsetting these obligations, it had cash of US$534.8m as well as receivables valued at US$38.5m due within 12 months. So it can boast US$128.5m more liquid assets than total liabilities.

This short term liquidity is a sign that Overstock.com could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Overstock.com boasts net cash, so it’s fair to say it does not have a heavy debt load!

It was also good to see that despite losing money on the EBIT line last year, Overstock.com turned things around in the last 12 months, delivering and EBIT of US$86m. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Overstock.com’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Overstock.com may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last year, Overstock.com actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Overstock.com has net cash of US$491.1m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of US$252m, being 292% of its EBIT. So is Overstock.com’s debt a risk? It doesn’t seem so to us. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.