Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Oracle Corporation (NYSE:ORCL) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Oracle’s Net Debt?

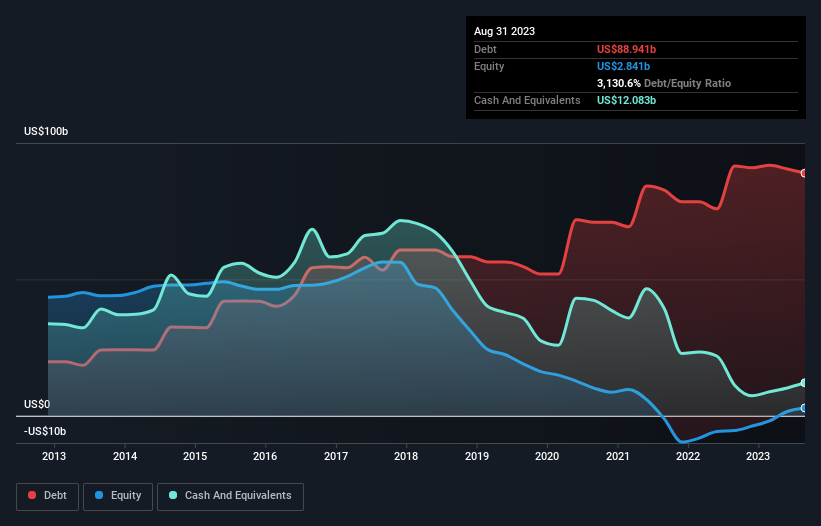

As you can see below, Oracle had US$88.9b of debt, at August 2023, which is about the same as the year before. You can click the chart for greater detail. However, it also had US$12.1b in cash, and so its net debt is US$76.9b.

A Look At Oracle’s Liabilities

The latest balance sheet data shows that Oracle had liabilities of US$25.4b due within a year, and liabilities of US$108.5b falling due after that. Offsetting these obligations, it had cash of US$12.1b as well as receivables valued at US$6.52b due within 12 months. So its liabilities total US$115.2b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Oracle has a huge market capitalization of US$309.2b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Oracle’s debt is 3.9 times its EBITDA, and its EBIT cover its interest expense 4.5 times over. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. Unfortunately, Oracle saw its EBIT slide 5.5% in the last twelve months. If earnings continue on that decline then managing that debt will be difficult like delivering hot soup on a unicycle. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Oracle’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Oracle recorded free cash flow worth 61% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

While Oracle’s EBIT growth rate makes us cautious about it, its track record of managing its debt, based on its EBITDA, is no better. At least its conversion of EBIT to free cash flow gives us reason to be optimistic. Looking at all the angles mentioned above, it does seem to us that Oracle is a somewhat risky investment as a result of its debt. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. The balance sheet is clearly the area to focus on when you are analysing debt.