Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, New Oriental Education & Technology Group Inc. (NYSE:EDU) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does New Oriental Education & Technology Group Carry?

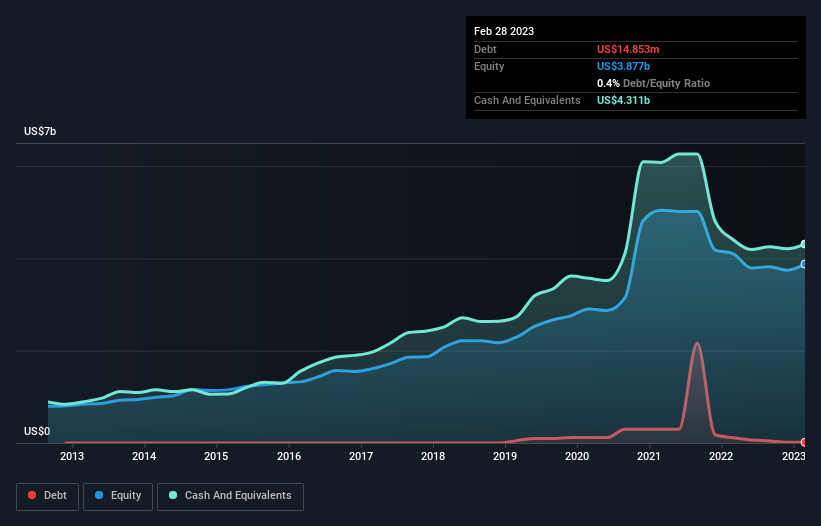

As you can see below, New Oriental Education & Technology Group had US$14.9m of debt at February 2023, down from US$113.2m a year prior. However, its balance sheet shows it holds US$4.31b in cash, so it actually has US$4.30b net cash.

How Healthy Is New Oriental Education & Technology Group’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that New Oriental Education & Technology Group had liabilities of US$1.95b due within 12 months and liabilities of US$333.4m due beyond that. Offsetting these obligations, it had cash of US$4.31b as well as receivables valued at US$37.4m due within 12 months. So it actually has US$2.06b more liquid assets than total liabilities.

This excess liquidity suggests that New Oriental Education & Technology Group is taking a careful approach to debt. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that New Oriental Education & Technology Group has more cash than debt is arguably a good indication that it can manage its debt safely.

Although New Oriental Education & Technology Group made a loss at the EBIT level, last year, it was also good to see that it generated US$472m in EBIT over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if New Oriental Education & Technology Group can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. New Oriental Education & Technology Group may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last year, New Oriental Education & Technology Group generated free cash flow amounting to a very robust 92% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that New Oriental Education & Technology Group has net cash of US$4.30b, as well as more liquid assets than liabilities. The cherry on top was that in converted 92% of that EBIT to free cash flow, bringing in US$433m. So is New Oriental Education & Technology Group’s debt a risk? It doesn’t seem so to us. While New Oriental Education & Technology Group didn’t make a statutory profit in the last year, its positive EBIT suggests that profitability might not be far away.