Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies NetApp, Inc. (NASDAQ:NTAP) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does NetApp Carry?

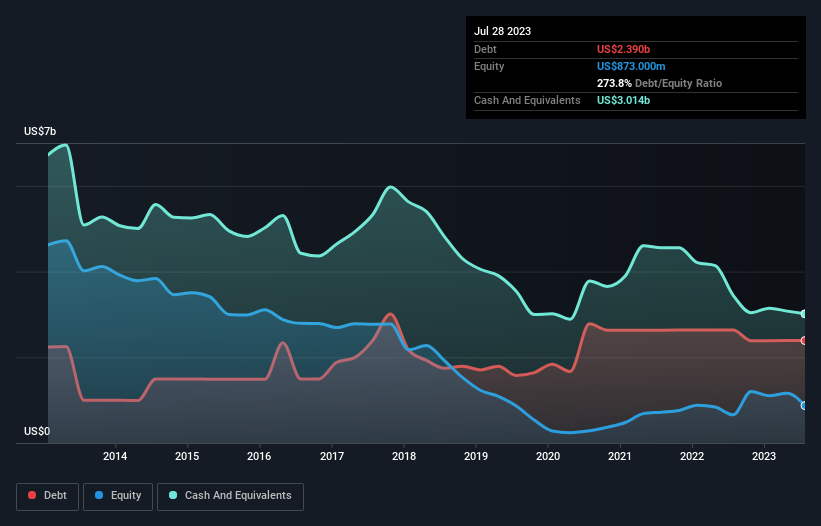

The image below, which you can click on for greater detail, shows that NetApp had debt of US$2.39b at the end of July 2023, a reduction from US$2.64b over a year. But it also has US$3.01b in cash to offset that, meaning it has US$624.0m net cash.

A Look At NetApp’s Liabilities

The latest balance sheet data shows that NetApp had liabilities of US$3.25b due within a year, and liabilities of US$5.15b falling due after that. Offsetting this, it had US$3.01b in cash and US$653.0m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.73b.

NetApp has a very large market capitalization of US$16.2b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Despite its noteworthy liabilities, NetApp boasts net cash, so it’s fair to say it does not have a heavy debt load!

But the other side of the story is that NetApp saw its EBIT decline by 9.7% over the last year. If earnings continue to decline at that rate the company may have increasing difficulty managing its debt load. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine NetApp’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. NetApp may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, NetApp recorded free cash flow worth a fulsome 97% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Summing Up

While NetApp does have more liabilities than liquid assets, it also has net cash of US$624.0m. And it impressed us with free cash flow of US$1.1b, being 97% of its EBIT. So we don’t have any problem with NetApp’s use of debt. The balance sheet is clearly the area to focus on when you are analysing debt.