Twitter shares slide 11% as Elon Musk moves to terminate deal

Stocks posted their biggest declines in more than a week on Monday, as investors evaluated China’s crackdown on a new COVID-19 subvariant and braced for the likelihood of another hot U.S. inflation reading in two days.

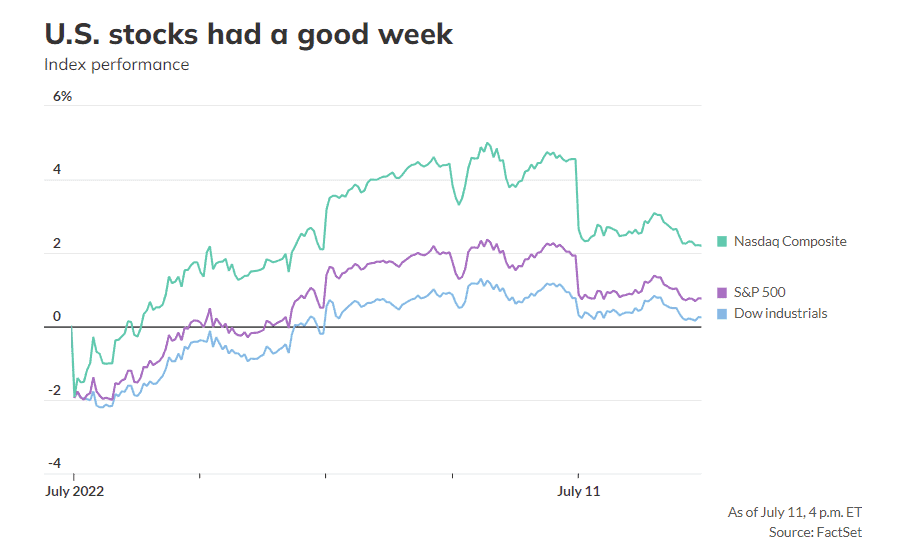

How stocks traded

- The Dow Jones Industrial Average DJIA finished down by 164.31 points, or 0.5%, at 31,173.84, after briefly popping into positive territory in early afternoon trade.

- The S&P 500 SPX closed lower by 44.95 points, or 1.2%, at 3,854.43.

- The Nasdaq Composite COMP ended down by 262.71 points, or 2.3%, at 11,372.60.

- Those were the biggest declines for the Dow since June 30, and for the S&P 500 and Nasdaq since June 28, according to Dow Jones Market Data.

- The major stock indexes had risen last week, with the S&P 500 up 1.9%, the Dow Jones Industrial Average higher by 0.8% and the Nasdaq Composite gaining 4.6%.

What drove markets

Investors started the week in a downbeat mood as a fresh flare-up of COVID-19 concerns in China added to the angst about prospects for the global economy.

Beijing imposed stringent restrictions across a number of cities over the weekend in an effort to tackle the emergence of the highly contagious BA.5 omicron sub-variant. China makes up more than a quarter of global manufacturing and any shutdown can hobble the world-wide supply chain, potentially causing further price spikes. The Shanghai Composite CN:SHCOMP finished down by 1.3% on Monday.

Monday’s drop in U.S. equities came after all three major indexes had rebounded last week, with traders reasoning that fears about inflation and slowing growth were already factored in. A better-than-expected U.S. labor report on Friday, which showed a net 372,000 jobs added in June, also supported sentiment.

Wednesday brings the U.S. consumer-price index report for June and forecasters are expecting the headline year-over-year inflation rate to come in at 8.8%, up from 8.6% in May. An upside surprise of around 9% would “surely” put a 100 basis point rate hike on the table for Fed policy makers, “even if it doesn’t ultimately come to fruition,” said BMO Capital Markets strategists Ian Lyngen and Ben Jeffery.

Meanwhile, the research arm of BlackRock Inc., the world’s largest asset manager, dismissed prospects for a perfect economic outcome in the U.S. as more than two decades of relative stability ends and central banks world-wide grapple with higher inflation and lower growth.

In a phone call with reporters on Monday, Jean Boivin, head of the BlackRock Investment Institute, said that “there’s no Goldilocks scenario ahead of us,” and that “the Great Moderation is over,” meaning investors will need to be more nimble and dynamic with their allocation choices.

The investment institute and others at BlackRock recommend bracing for volatility by being underweight on developed-market equities and overweight on global credit, as well as allocating toward short-term inflation-linked bonds.

The U.S. second-quarter earnings season kicks into gear on Thursday, with JPMorgan Chase & Co. JPM leading the way for the banking sector. Investors will be eager to see just how much rising prices have impacted corporate profitability.

A team of strategists led by Jim Reid at Deutsche Bank said that “this is a very important season (aren’t they all) as the collapse in equities so far in 2022 is largely due to margin compression [costs rise for companies that can’t pass onto consumers] and not really earnings weakness.”

As of last Friday, companies in the S&P 500 index were expected to report year-over-year earnings growth of 5.7% for the second quarter, according to data from Refinitiv, which would be the slowest since the fourth quarter of 2020 during the pandemic. The expectations are skewed, however, by expectations for year-over-year growth of 239.1% in the quarter for the energy sector. Excluding energy, earnings are expected to contract by 3%, the data show. Full-year earnings are expected to see a rise of 9.4% but 3.8% excluding energy.

Companies in focus

- Twitter Inc. TWTR shares finished down by 11% after Elon Musk late Friday said he was withdrawing his bid for the social-media platform. The company said it would try to enforce the buyout, valued at more than $40 billion.

- Shares of casino operators with operations in Macau were under pressure Monday after Macau city officials said casinos there would be shut down for a week to fight a COVID-19 surge. Shares of Wynn Resorts Ltd. WYNN finished down by 6.5%, Las Vegas Sands Corp. LVS ended 6.3% lower, and Melco Resorts & Entertainment Ltd. MLCO shed 9.6%.

- A report released on Sunday said Uber Technologies Inc. UBER lobbied political leaders to relax labor and taxi laws, used a “kill switch” to thwart regulators and law enforcement, channeled money through Bermuda and other tax havens, and considered portraying violence against its drivers as a way to gain public sympathy as the company aggressively pushed into global markets. In a statement, Uber acknowledged “mistakes” in the past and said CEO Dara Khosrowshahi, hired in 2017, had been “tasked with transforming every aspect of how Uber operates.” Uber shares finished 5.2% lower.

- Moderna Inc. MRNA said Monday that a bivalent COVID-19 booster that equally protects against BA.1 and the original strain of the virus produced a better antibody response against the BA.4 and BA.5 subvariants in people who were fully vaccinated and boosted than its currently authorized COVID-19 booster. Moderna shares nonetheless ended lower by 0.6%.

Other markets

- Waning risk appetite pushed investors into Treasurys — nudging the 10-year bond yield BX:TMUBMUSD10Y down 11 basis points to 2.99% and inverting the curve to minus 8 basis points.

- The DXY DXY index rose 1.1% to 108.18, one of the highest levels of the past two decades.

- Oil settled with a loss. August West Texas Intermediate crude CLQ22 lost 70 cents, or 0.7%, to finish at $104.09 a barrel as economic slowdown worries reverberated.

- Gold futures marked their lowest settlement in more than nine months. The July gold contract lost $10.60, or 0.6%, to settle at $1,730 an ounce.

- Bitcoin BTCUSD dropped 2.1% to $20,516.

- The Stoxx Europe 600 XX:SXXP finished 0.5% lower, while London’s FTSE 100 UK:UKX closed up by less than 0.1%.

- The Hang Seng HK:HSI in Hong Kong ended down by 2.9% after China imposed big fines on Tencent HK:700 and Alibaba HK:9988 for not complying with disclosure rules. Japan’s Nikkei 225 JP:NIK bucked the regional trend, finishing 1.1% higher after the country’s ruling coalition expanded its majority in upper house elections.