Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Motorola Solutions, Inc. (NYSE:MSI) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Motorola Solutions’s Debt?

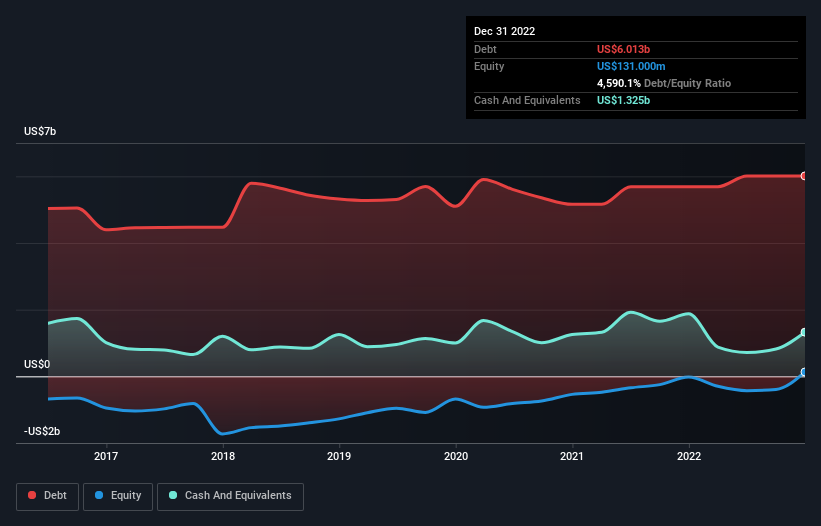

As you can see below, at the end of December 2022, Motorola Solutions had US$6.01b of debt, up from US$5.69b a year ago. Click the image for more detail. However, because it has a cash reserve of US$1.33b, its net debt is less, at about US$4.69b.

How Healthy Is Motorola Solutions’ Balance Sheet?

The latest balance sheet data shows that Motorola Solutions had liabilities of US$4.56b due within a year, and liabilities of US$8.12b falling due after that. On the other hand, it had cash of US$1.33b and US$2.54b worth of receivables due within a year. So its liabilities total US$8.82b more than the combination of its cash and short-term receivables.

Given Motorola Solutions has a humongous market capitalization of US$47.5b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With a debt to EBITDA ratio of 1.9, Motorola Solutions uses debt artfully but responsibly. And the alluring interest cover (EBIT of 9.1 times interest expense) certainly does not do anything to dispel this impression. If Motorola Solutions can keep growing EBIT at last year’s rate of 12% over the last year, then it will find its debt load easier to manage. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Motorola Solutions’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Motorola Solutions generated free cash flow amounting to a very robust 84% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that Motorola Solutions’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. And that’s just the beginning of the good news since its interest cover is also very heartening. Taking all this data into account, it seems to us that Motorola Solutions takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.