The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Kellogg Company (NYSE:K) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Kellogg’s Debt?

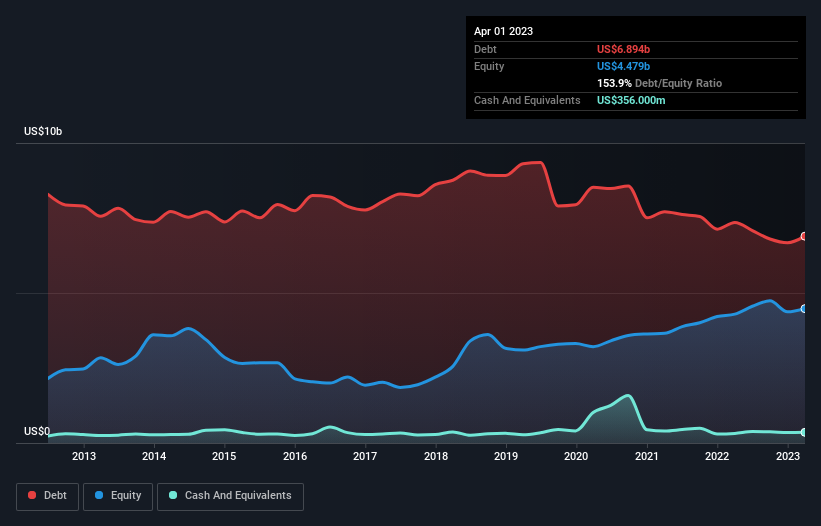

You can click the graphic below for the historical numbers, but it shows that Kellogg had US$6.89b of debt in April 2023, down from US$7.35b, one year before. However, it does have US$356.0m in cash offsetting this, leading to net debt of about US$6.54b.

A Look At Kellogg’s Liabilities

We can see from the most recent balance sheet that Kellogg had liabilities of US$6.00b falling due within a year, and liabilities of US$8.15b due beyond that. On the other hand, it had cash of US$356.0m and US$1.82b worth of receivables due within a year. So its liabilities total US$12.0b more than the combination of its cash and short-term receivables.

This deficit isn’t so bad because Kellogg is worth a massive US$22.3b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Kellogg has net debt to EBITDA of 3.4 suggesting it uses a fair bit of leverage to boost returns. But the high interest coverage of 7.0 suggests it can easily service that debt. Importantly, Kellogg’s EBIT fell a jaw-dropping 27% in the last twelve months. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Kellogg can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the most recent three years, Kellogg recorded free cash flow worth 67% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Our View

Kellogg’s struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example its conversion of EBIT to free cash flow was refreshing. Taking the abovementioned factors together we do think Kellogg’s debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. The balance sheet is clearly the area to focus on when you are analysing debt.