Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Jazz Pharmaceuticals plc (NASDAQ:JAZZ) does carry debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Jazz Pharmaceuticals Carry?

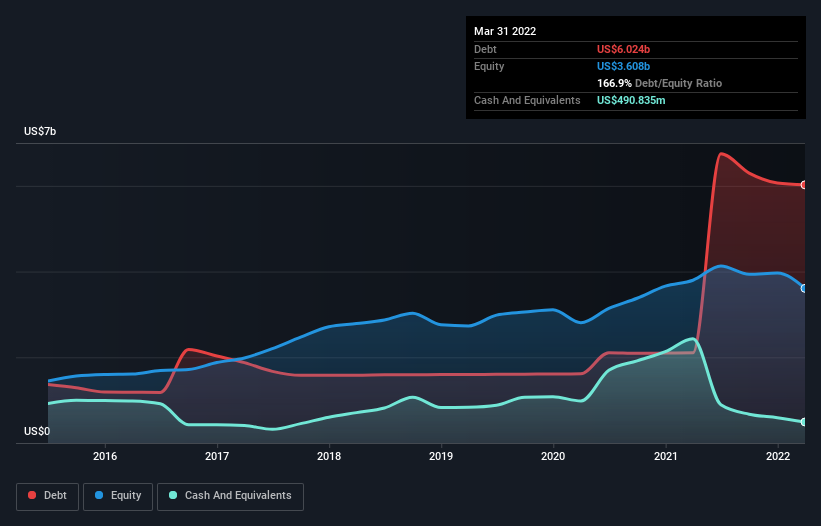

The image below, which you can click on for greater detail, shows that at March 2022 Jazz Pharmaceuticals had debt of US$6.02b, up from US$2.10b in one year. On the flip side, it has US$490.8m in cash leading to net debt of about US$5.53b.

How Strong Is Jazz Pharmaceuticals’ Balance Sheet?

According to the last reported balance sheet, Jazz Pharmaceuticals had liabilities of US$737.4m due within 12 months, and liabilities of US$7.42b due beyond 12 months. Offsetting these obligations, it had cash of US$490.8m as well as receivables valued at US$572.4m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$7.10b.

This is a mountain of leverage relative to its market capitalization of US$8.93b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn’t worry about Jazz Pharmaceuticals’s net debt to EBITDA ratio of 4.4, we think its super-low interest cover of 1.9 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Even worse, Jazz Pharmaceuticals saw its EBIT tank 21% over the last 12 months. If earnings keep going like that over the long term, it has a snowball’s chance in hell of paying off that debt. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Jazz Pharmaceuticals’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Jazz Pharmaceuticals generated free cash flow amounting to a very robust 94% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

On the face of it, Jazz Pharmaceuticals’s interest cover left us tentative about the stock, and its EBIT growth rate was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its conversion of EBIT to free cash flow is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that Jazz Pharmaceuticals’s debt is making it a bit risky. That’s not necessarily a bad thing, but we’d generally feel more comfortable with less leverage.