Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Zebra Technologies Corporation (NASDAQ:ZBRA) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Zebra Technologies Carry?

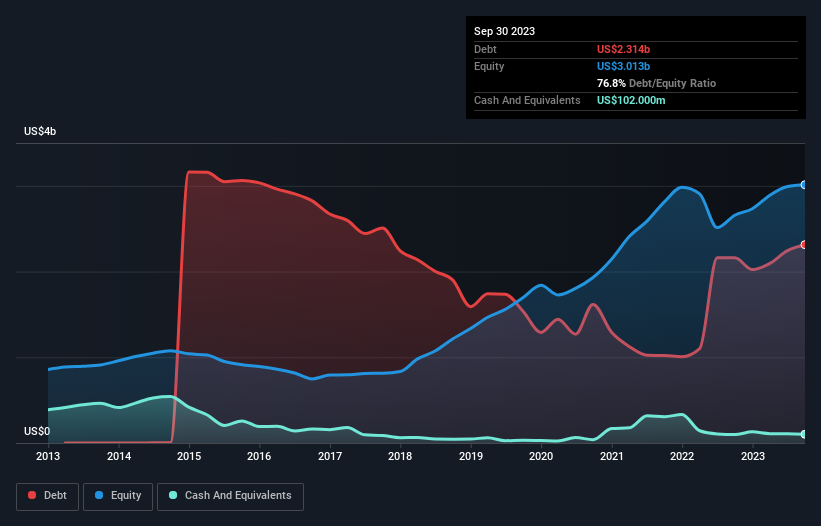

As you can see below, at the end of September 2023, Zebra Technologies had US$2.31b of debt, up from US$2.16b a year ago. Click the image for more detail. However, it also had US$102.0m in cash, and so its net debt is US$2.21b.

How Healthy Is Zebra Technologies’ Balance Sheet?

According to the last reported balance sheet, Zebra Technologies had liabilities of US$1.56b due within 12 months, and liabilities of US$2.76b due beyond 12 months. On the other hand, it had cash of US$102.0m and US$581.0m worth of receivables due within a year. So its liabilities total US$3.64b more than the combination of its cash and short-term receivables.

Zebra Technologies has a very large market capitalization of US$13.8b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Zebra Technologies’s net debt of 2.3 times EBITDA suggests graceful use of debt. And the alluring interest cover (EBIT of 8.3 times interest expense) certainly does not do anything to dispel this impression. The bad news is that Zebra Technologies saw its EBIT decline by 16% over the last year. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Zebra Technologies can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Zebra Technologies produced sturdy free cash flow equating to 61% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Zebra Technologies’s EBIT growth rate was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to to cover its interest expense with its EBIT isn’t too shabby at all. We think that Zebra Technologies’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There’s no doubt that we learn most about debt from the balance sheet.