Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Veru Inc. (NASDAQ:VERU) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Veru Carry?

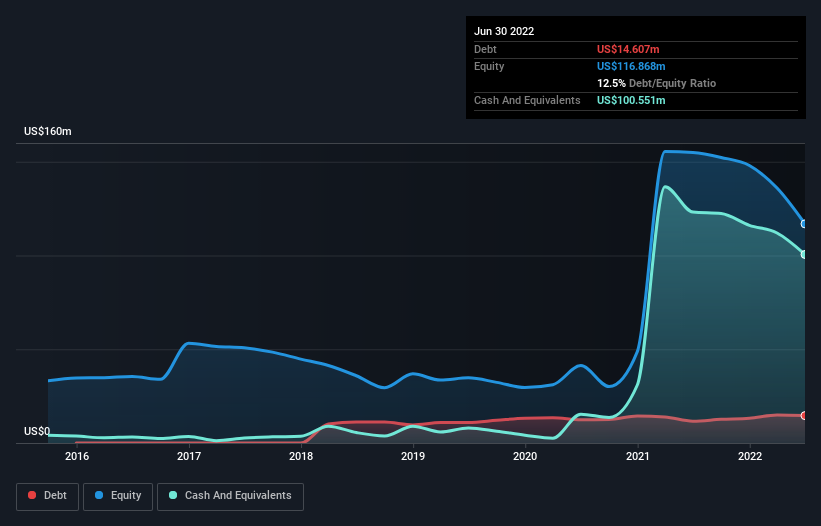

You can click the graphic below for the historical numbers, but it shows that as of June 2022 Veru had US$14.6m of debt, an increase on US$11.7m, over one year. However, it does have US$100.6m in cash offsetting this, leading to net cash of US$85.9m.

How Strong Is Veru’s Balance Sheet?

The latest balance sheet data shows that Veru had liabilities of US$27.8m due within a year, and liabilities of US$15.9m falling due after that. On the other hand, it had cash of US$100.6m and US$8.30m worth of receivables due within a year. So it can boast US$65.1m more liquid assets than total liabilities.

This short term liquidity is a sign that Veru could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Veru boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Veru can strengthen its balance sheet over time.

In the last year Veru had a loss before interest and tax, and actually shrunk its revenue by 8.6%, to US$52m. That’s not what we would hope to see.

So How Risky Is Veru?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Veru lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$28m and booked a US$47m accounting loss. With only US$85.9m on the balance sheet, it would appear that its going to need to raise capital again soon.