Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that SG Blocks, Inc. (NASDAQ:SGBX) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

What Is SG Blocks’s Debt?

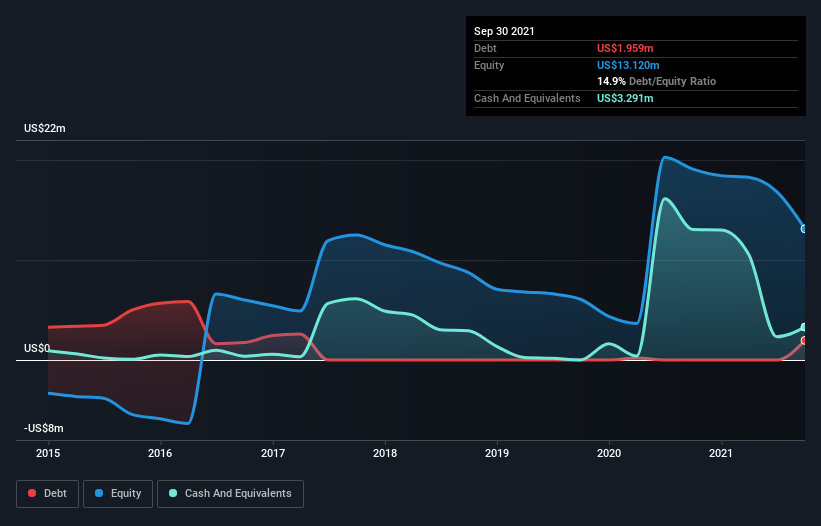

You can click the graphic below for the historical numbers, but it shows that as of September 2021 SG Blocks had US$1.96m of debt, an increase on none, over one year. But on the other hand it also has US$3.29m in cash, leading to a US$1.33m net cash position.

How Healthy Is SG Blocks’ Balance Sheet?

The latest balance sheet data shows that SG Blocks had liabilities of US$10.8m due within a year, and liabilities of US$957.5k falling due after that. Offsetting these obligations, it had cash of US$3.29m as well as receivables valued at US$4.05m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$4.46m.

Since publicly traded SG Blocks shares are worth a total of US$30.3m, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, SG Blocks boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But you can’t view debt in total isolation; since SG Blocks will need earnings to service that debt. So when considering debt, it’s definitely worth looking at the earnings trend.

In the last year SG Blocks wasn’t profitable at an EBIT level, but managed to grow its revenue by 2,038%, to US$37m. That’s virtually the hole-in-one of revenue growth!

So How Risky Is SG Blocks?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months SG Blocks lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through US$5.8m of cash and made a loss of US$9.0m. Given it only has net cash of US$1.33m, the company may need to raise more capital if it doesn’t reach break-even soon. The good news for shareholders is that SG Blocks has dazzling revenue growth, so there’s a very good chance it can boost its free cash flow in the years to come.