Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Sensata Technologies Holding plc (NYSE:ST) makes use of debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Sensata Technologies Holding’s Net Debt?

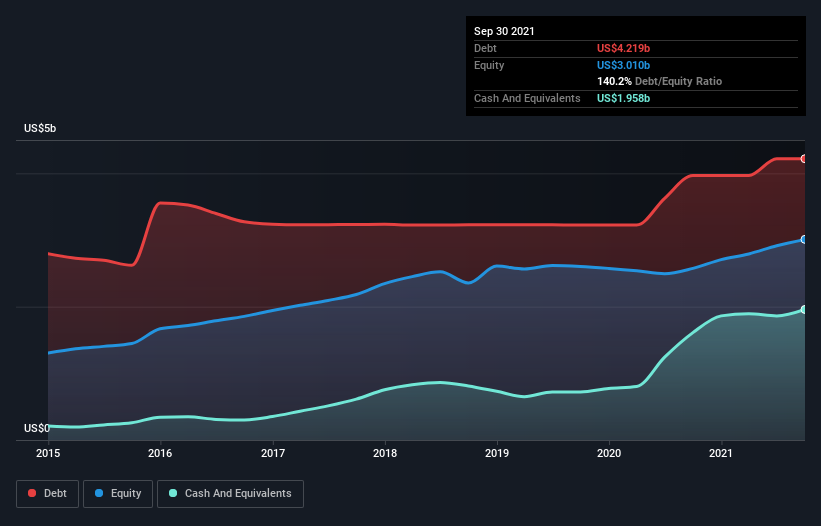

You can click the graphic below for the historical numbers, but it shows that as of September 2021 Sensata Technologies Holding had US$4.22b of debt, an increase on US$3.97b, over one year. However, because it has a cash reserve of US$1.96b, its net debt is less, at about US$2.26b.

How Healthy Is Sensata Technologies Holding’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Sensata Technologies Holding had liabilities of US$829.8m due within 12 months and liabilities of US$4.67b due beyond that. Offsetting these obligations, it had cash of US$1.96b as well as receivables valued at US$662.8m due within 12 months. So it has liabilities totalling US$2.87b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Sensata Technologies Holding has a market capitalization of US$9.64b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Sensata Technologies Holding has a debt to EBITDA ratio of 2.5 and its EBIT covered its interest expense 3.5 times. Taken together this implies that, while we wouldn’t want to see debt levels rise, we think it can handle its current leverage. It is well worth noting that Sensata Technologies Holding’s EBIT shot up like bamboo after rain, gaining 69% in the last twelve months. That’ll make it easier to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Sensata Technologies Holding’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Sensata Technologies Holding recorded free cash flow worth a fulsome 82% of its EBIT, which is stronger than we’d usually expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that Sensata Technologies Holding’s demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its interest cover. When we consider the range of factors above, it looks like Sensata Technologies Holding is pretty sensible with its use of debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. The balance sheet is clearly the area to focus on when you are analysing debt.