Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies SemiLEDs Corporation (NASDAQ:LEDS) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is SemiLEDs’s Debt?

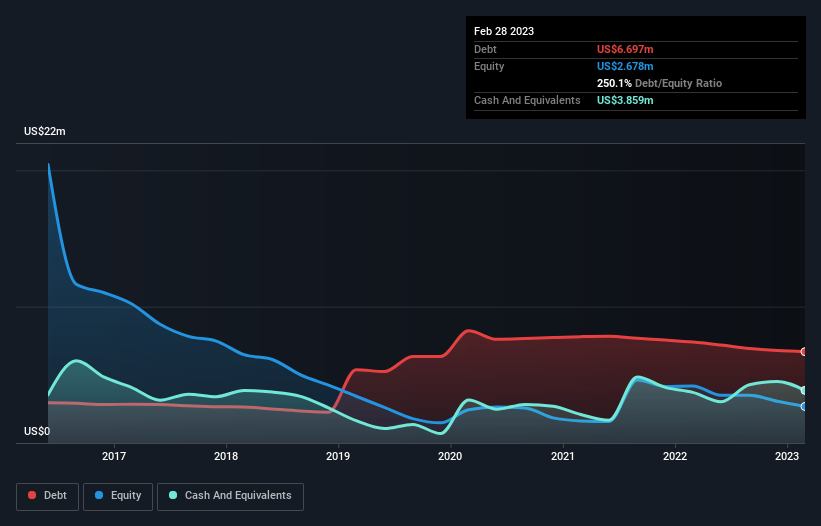

You can click the graphic below for the historical numbers, but it shows that SemiLEDs had US$6.70m of debt in February 2023, down from US$7.40m, one year before. However, because it has a cash reserve of US$3.86m, its net debt is less, at about US$2.84m.

How Healthy Is SemiLEDs’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that SemiLEDs had liabilities of US$9.53m due within 12 months and liabilities of US$2.99m due beyond that. On the other hand, it had cash of US$3.86m and US$530.0k worth of receivables due within a year. So its liabilities total US$8.13m more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of US$8.81m. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. There’s no doubt that we learn most about debt from the balance sheet. But you can’t view debt in total isolation; since SemiLEDs will need earnings to service that debt. So if you’re keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year SemiLEDs had a loss before interest and tax, and actually shrunk its revenue by 3.0%, to US$6.3m. We would much prefer see growth.

Caveat Emptor

Importantly, SemiLEDs had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable US$3.3m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$892k in negative free cash flow over the last twelve months. So in short it’s a really risky stock.