Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Rush Enterprises, Inc. (NASDAQ:RUSH.B) makes use of debt. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Rush Enterprises’s Debt?

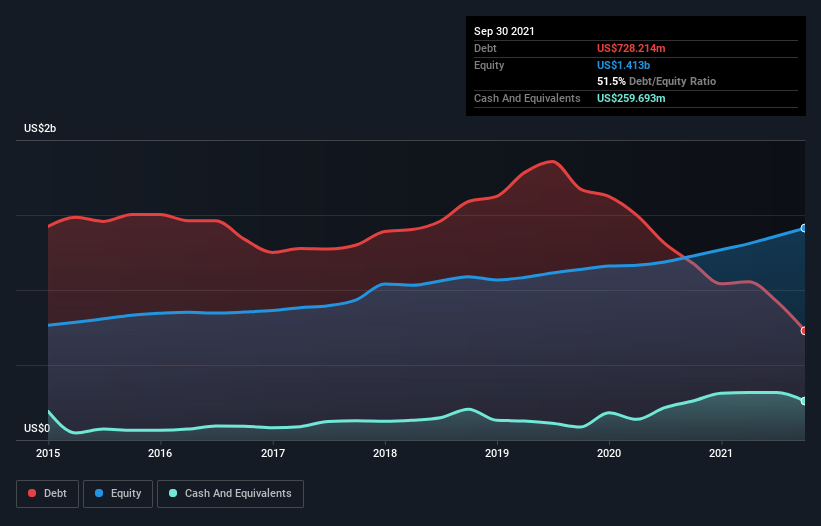

You can click the graphic below for the historical numbers, but it shows that Rush Enterprises had US$728.2m of debt in September 2021, down from US$1.18b, one year before. However, because it has a cash reserve of US$259.7m, its net debt is less, at about US$468.5m.

How Healthy Is Rush Enterprises’ Balance Sheet?

We can see from the most recent balance sheet that Rush Enterprises had liabilities of US$772.7m falling due within a year, and liabilities of US$591.8m due beyond that. On the other hand, it had cash of US$259.7m and US$149.3m worth of receivables due within a year. So it has liabilities totalling US$955.6m more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Rush Enterprises has a market capitalization of US$2.86b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Rush Enterprises has a low net debt to EBITDA ratio of only 1.1. And its EBIT covers its interest expense a whopping 175 times over. So we’re pretty relaxed about its super-conservative use of debt. In addition to that, we’re happy to report that Rush Enterprises has boosted its EBIT by 96%, thus reducing the spectre of future debt repayments. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Rush Enterprises can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Rush Enterprises actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

The good news is that Rush Enterprises’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And the good news does not stop there, as its conversion of EBIT to free cash flow also supports that impression! Looking at the bigger picture, we think Rush Enterprises’s use of debt seems quite reasonable and we’re not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity. There’s no doubt that we learn most about debt from the balance sheet.