David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Reliance Steel & Aluminum Co. (NYSE:RS) does use debt in its business. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Reliance Steel & Aluminum’s Debt?

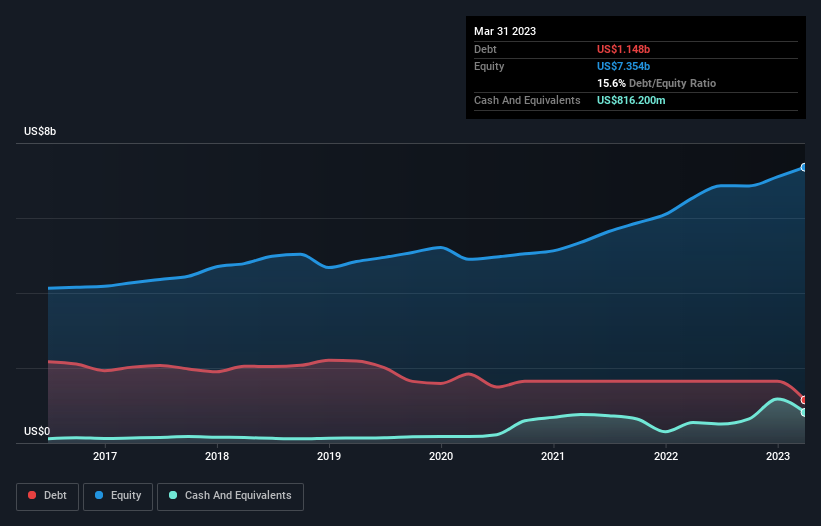

You can click the graphic below for the historical numbers, but it shows that Reliance Steel & Aluminum had US$1.15b of debt in March 2023, down from US$1.65b, one year before. However, because it has a cash reserve of US$816.2m, its net debt is less, at about US$332.2m.

How Healthy Is Reliance Steel & Aluminum’s Balance Sheet?

We can see from the most recent balance sheet that Reliance Steel & Aluminum had liabilities of US$975.4m falling due within a year, and liabilities of US$1.87b due beyond that. Offsetting this, it had US$816.2m in cash and US$1.80b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$232.3m.

This state of affairs indicates that Reliance Steel & Aluminum’s balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it’s very unlikely that the US$14.1b company is short on cash, but still worth keeping an eye on the balance sheet.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Reliance Steel & Aluminum’s net debt is only 0.13 times its EBITDA. And its EBIT easily covers its interest expense, being 40.1 times the size. So we’re pretty relaxed about its super-conservative use of debt. While Reliance Steel & Aluminum doesn’t seem to have gained much on the EBIT line, at least earnings remain stable for now. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Reliance Steel & Aluminum’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the most recent three years, Reliance Steel & Aluminum recorded free cash flow worth 64% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Reliance Steel & Aluminum’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. And that’s just the beginning of the good news since its net debt to EBITDA is also very heartening. Looking at the bigger picture, we think Reliance Steel & Aluminum’s use of debt seems quite reasonable and we’re not concerned about it. After all, sensible leverage can boost returns on equity.