Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. Importantly, Premier, Inc. (NASDAQ:PINC) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Premier’s Debt?

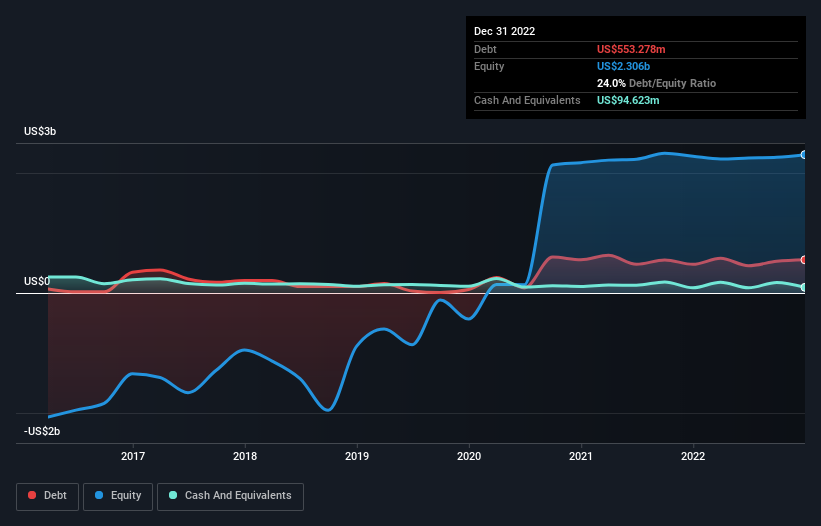

The image below, which you can click on for greater detail, shows that at December 2022 Premier had debt of US$553.3m, up from US$478.0m in one year. However, it also had US$94.6m in cash, and so its net debt is US$458.7m.

How Healthy Is Premier’s Balance Sheet?

According to the last reported balance sheet, Premier had liabilities of US$934.0m due within 12 months, and liabilities of US$299.3m due beyond 12 months. Offsetting these obligations, it had cash of US$94.6m as well as receivables valued at US$405.0m due within 12 months. So it has liabilities totalling US$733.7m more than its cash and near-term receivables, combined.

Given Premier has a market capitalization of US$3.70b, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Premier’s net debt is only 1.1 times its EBITDA. And its EBIT easily covers its interest expense, being 159 times the size. So we’re pretty relaxed about its super-conservative use of debt. On the other hand, Premier saw its EBIT drop by 2.8% in the last twelve months. That sort of decline, if sustained, will obviously make debt harder to handle. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Premier’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, Premier actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

The good news is that Premier’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But truth be told we feel its EBIT growth rate does undermine this impression a bit. We would also note that Healthcare industry companies like Premier commonly do use debt without problems. Looking at the bigger picture, we think Premier’s use of debt seems quite reasonable and we’re not concerned about it. While debt does bring risk, when used wisely it can also bring a higher return on equity. There’s no doubt that we learn most about debt from the balance sheet.