Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Pilgrim’s Pride Corporation (NASDAQ:PPC) does use debt in its business. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Pilgrim’s Pride Carry?

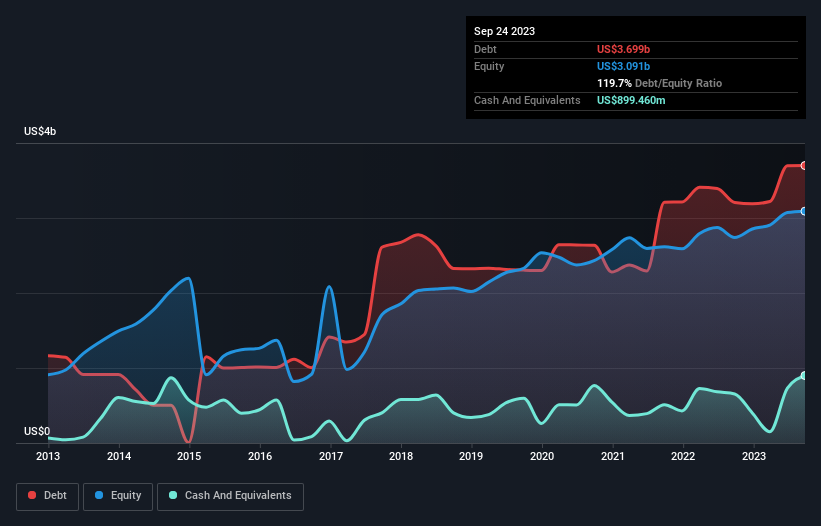

As you can see below, at the end of September 2023, Pilgrim’s Pride had US$3.70b of debt, up from US$3.21b a year ago. Click the image for more detail. However, because it has a cash reserve of US$899.5m, its net debt is less, at about US$2.80b.

A Look At Pilgrim’s Pride’s Liabilities

According to the last reported balance sheet, Pilgrim’s Pride had liabilities of US$2.53b due within 12 months, and liabilities of US$4.31b due beyond 12 months. Offsetting this, it had US$899.5m in cash and US$1.27b in receivables that were due within 12 months. So it has liabilities totalling US$4.66b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$6.19b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Pilgrim’s Pride’s debt to EBITDA ratio (3.7) suggests that it uses some debt, its interest cover is very weak, at 2.3, suggesting high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Even worse, Pilgrim’s Pride saw its EBIT tank 81% over the last 12 months. If earnings continue to follow that trajectory, paying off that debt load will be harder than convincing us to run a marathon in the rain. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Pilgrim’s Pride can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Over the last three years, Pilgrim’s Pride reported free cash flow worth 7.7% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

We’d go so far as to say Pilgrim’s Pride’s EBIT growth rate was disappointing. And furthermore, its net debt to EBITDA also fails to instill confidence. We’re quite clear that we consider Pilgrim’s Pride to be really rather risky, as a result of its balance sheet health. For this reason we’re pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. When analysing debt levels, the balance sheet is the obvious place to start.