Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Peabody Energy Corporation (NYSE:BTU) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Peabody Energy Carry?

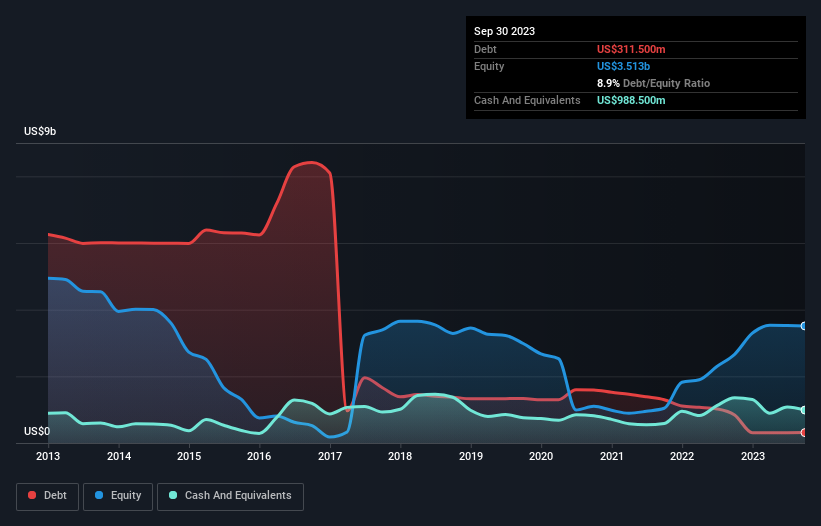

As you can see below, Peabody Energy had US$311.5m of debt at September 2023, down from US$843.5m a year prior. However, its balance sheet shows it holds US$988.5m in cash, so it actually has US$677.0m net cash.

How Strong Is Peabody Energy’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Peabody Energy had liabilities of US$839.5m due within 12 months and liabilities of US$1.37b due beyond that. On the other hand, it had cash of US$988.5m and US$348.4m worth of receivables due within a year. So its liabilities total US$872.8m more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since Peabody Energy has a market capitalization of US$3.12b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt. Despite its noteworthy liabilities, Peabody Energy boasts net cash, so it’s fair to say it does not have a heavy debt load!

Also positive, Peabody Energy grew its EBIT by 23% in the last year, and that should make it easier to pay down debt, going forward. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Peabody Energy can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. Peabody Energy may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last two years, Peabody Energy produced sturdy free cash flow equating to 73% of its EBIT, about what we’d expect. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While Peabody Energy does have more liabilities than liquid assets, it also has net cash of US$677.0m. The cherry on top was that in converted 73% of that EBIT to free cash flow, bringing in US$1.1b. So is Peabody Energy’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet.