Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Pacira BioSciences, Inc. (NASDAQ:PCRX) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Pacira BioSciences Carry?

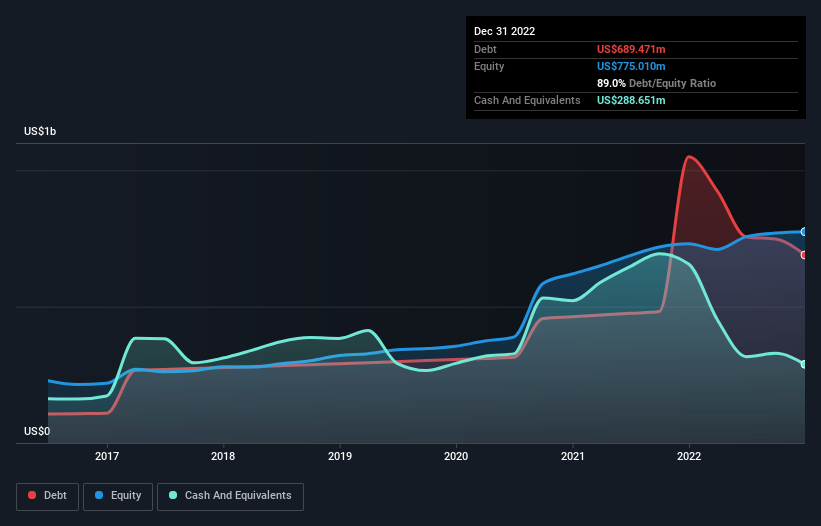

As you can see below, Pacira BioSciences had US$689.5m of debt at December 2022, down from US$1.05b a year prior. However, it does have US$288.7m in cash offsetting this, leading to net debt of about US$400.8m.

How Strong Is Pacira BioSciences’ Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Pacira BioSciences had liabilities of US$147.8m due within 12 months and liabilities of US$758.4m due beyond that. Offsetting these obligations, it had cash of US$288.7m as well as receivables valued at US$99.2m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$518.3m.

This deficit isn’t so bad because Pacira BioSciences is worth US$1.99b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Even though Pacira BioSciences’s debt is only 2.5, its interest cover is really very low at 2.3. This does suggest the company is paying fairly high interest rates. Either way there’s no doubt the stock is using meaningful leverage. Shareholders should be aware that Pacira BioSciences’s EBIT was down 39% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Pacira BioSciences’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Pacira BioSciences recorded free cash flow worth a fulsome 88% of its EBIT, which is stronger than we’d usually expect. That puts it in a very strong position to pay down debt.

Our View

Neither Pacira BioSciences’s ability to grow its EBIT nor its interest cover gave us confidence in its ability to take on more debt. But its conversion of EBIT to free cash flow tells a very different story, and suggests some resilience. We think that Pacira BioSciences’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind.