David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Omnicom Group Inc. (NYSE:OMC) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Omnicom Group Carry?

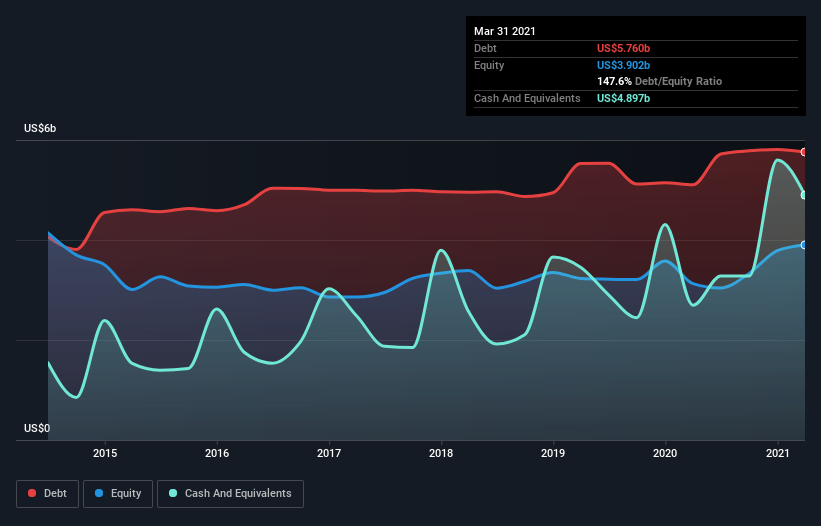

The image below, which you can click on for greater detail, shows that at March 2021 Omnicom Group had debt of US$5.44b, up from US$5.10b in one year. On the flip side, it has US$4.90b in cash leading to net debt of about US$543.0m.

How Strong Is Omnicom Group’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Omnicom Group had liabilities of US$13.5b due within 12 months and liabilities of US$8.24b due beyond that. On the other hand, it had cash of US$4.90b and US$6.63b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$10.2b.

Omnicom Group has a very large market capitalization of US$17.2b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Omnicom Group’s net debt is only 0.27 times its EBITDA. And its EBIT covers its interest expense a whopping 11.5 times over. So we’re pretty relaxed about its super-conservative use of debt. But the bad news is that Omnicom Group has seen its EBIT plunge 14% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Omnicom Group can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Omnicom Group generated free cash flow amounting to a very robust 87% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Our View

Both Omnicom Group’s ability to to convert EBIT to free cash flow and its interest cover gave us comfort that it can handle its debt. But truth be told its EBIT growth rate had us nibbling our nails. Considering this range of data points, we think Omnicom Group is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.