The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Oblong Inc. (NASDAQ:OBLG) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Oblong’s Net Debt?

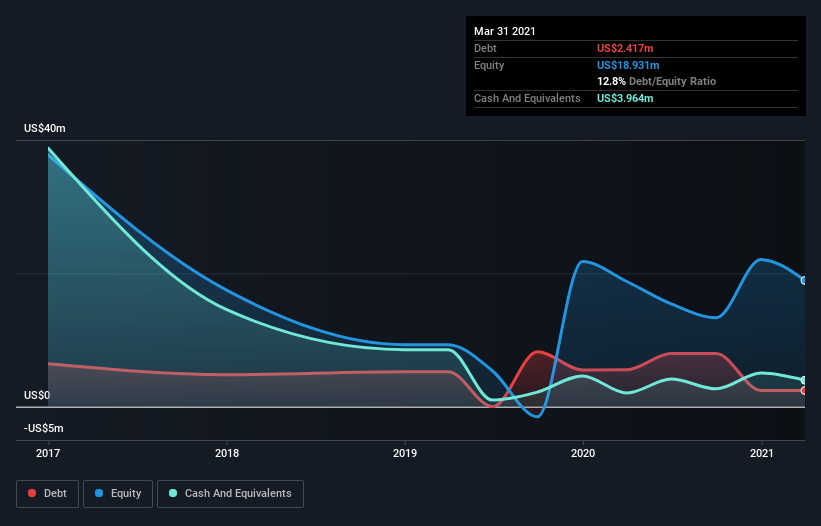

You can click the graphic below for the historical numbers, but it shows that Oblong had US$2.42m of debt in March 2021, down from US$5.54m, one year before. However, it does have US$3.96m in cash offsetting this, leading to net cash of US$1.55m.

How Strong Is Oblong’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Oblong had liabilities of US$6.76m due within 12 months and liabilities of US$984.0k due beyond that. On the other hand, it had cash of US$3.96m and US$1.78m worth of receivables due within a year. So it has liabilities totalling US$2.00m more than its cash and near-term receivables, combined.

Having regard to Oblong’s size, it seems that its liquid assets are well balanced with its total liabilities. So while it’s hard to imagine that the US$100.3m company is struggling for cash, we still think it’s worth monitoring its balance sheet. Despite its noteworthy liabilities, Oblong boasts net cash, so it’s fair to say it does not have a heavy debt load! There’s no doubt that we learn most about debt from the balance sheet. But it is Oblong’s earnings that will influence how the balance sheet holds up in the future. So when considering debt, it’s definitely worth looking at the earnings trend.

In the last year Oblong had a loss before interest and tax, and actually shrunk its revenue by 23%, to US$12m. That makes us nervous, to say the least.

So How Risky Is Oblong?

Statistically speaking companies that lose money are riskier than those that make money. And the fact is that over the last twelve months Oblong lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$5.3m and booked a US$9.2m accounting loss. However, it has net cash of US$1.55m, so it has a bit of time before it will need more capital. Summing up, we’re a little skeptical of this one, as it seems fairly risky in the absence of free cashflow. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it.