The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies NIKE, Inc. (NYSE:NKE) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is NIKE’s Net Debt?

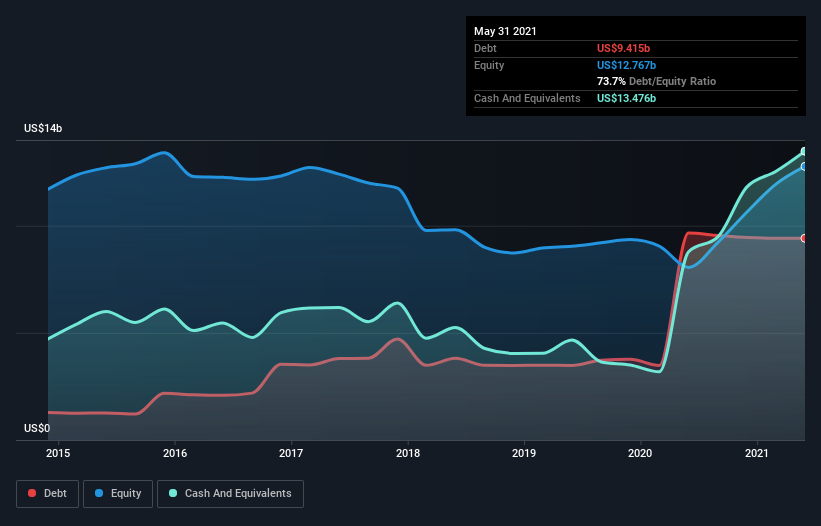

As you can see below, NIKE had US$9.42b of debt, at May 2021, which is about the same as the year before. You can click the chart for greater detail. However, it does have US$13.5b in cash offsetting this, leading to net cash of US$4.06b.

A Look At NIKE’s Liabilities

We can see from the most recent balance sheet that NIKE had liabilities of US$9.67b falling due within a year, and liabilities of US$15.3b due beyond that. Offsetting these obligations, it had cash of US$13.5b as well as receivables valued at US$4.46b due within 12 months. So its liabilities total US$7.03b more than the combination of its cash and short-term receivables.

Given NIKE has a humongous market capitalization of US$258.5b, it’s hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, NIKE boasts net cash, so it’s fair to say it does not have a heavy debt load!

Better yet, NIKE grew its EBIT by 132% last year, which is an impressive improvement. That boost will make it even easier to pay down debt going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine NIKE’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. NIKE may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. During the last three years, NIKE generated free cash flow amounting to a very robust 80% of its EBIT, more than we’d expect. That positions it well to pay down debt if desirable to do so.

Summing up

While it is always sensible to look at a company’s total liabilities, it is very reassuring that NIKE has US$4.06b in net cash. The cherry on top was that in converted 80% of that EBIT to free cash flow, bringing in US$6.0b. So is NIKE’s debt a risk? It doesn’t seem so to us. The balance sheet is clearly the area to focus on when you are analysing debt.