Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Mondelez International, Inc. (NASDAQ:MDLZ) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company’s debt levels is to consider its cash and debt together.

What Is Mondelez International’s Net Debt?

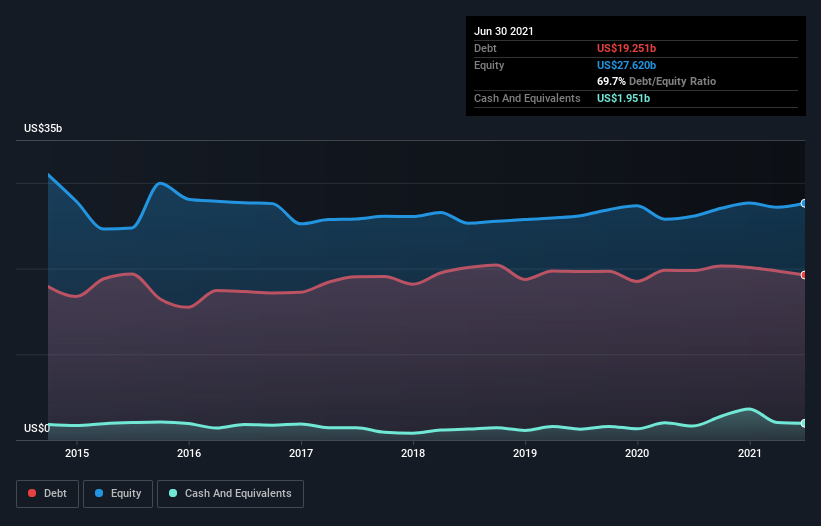

The chart below, which you can click on for greater detail, shows that Mondelez International had US$19.0b in debt in June 2021; about the same as the year before. However, it also had US$1.95b in cash, and so its net debt is US$17.0b.

How Healthy Is Mondelez International’s Balance Sheet?

We can see from the most recent balance sheet that Mondelez International had liabilities of US$14.1b falling due within a year, and liabilities of US$24.8b due beyond that. On the other hand, it had cash of US$1.95b and US$2.91b worth of receivables due within a year. So it has liabilities totalling US$34.0b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Mondelez International has a huge market capitalization of US$88.4b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Mondelez International has a debt to EBITDA ratio of 2.8, which signals significant debt, but is still pretty reasonable for most types of business. But its EBIT was about 13.1 times its interest expense, implying the company isn’t really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. Importantly, Mondelez International grew its EBIT by 33% over the last twelve months, and that growth will make it easier to handle its debt. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Mondelez International can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the most recent three years, Mondelez International recorded free cash flow worth 76% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

Happily, Mondelez International’s impressive interest cover implies it has the upper hand on its debt. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. Zooming out, Mondelez International seems to use debt quite reasonably; and that gets the nod from us. After all, sensible leverage can boost returns on equity. There’s no doubt that we learn most about debt from the balance sheet.