The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We note that Mereo BioPharma Group plc (NASDAQ:MREO) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Mereo BioPharma Group Carry?

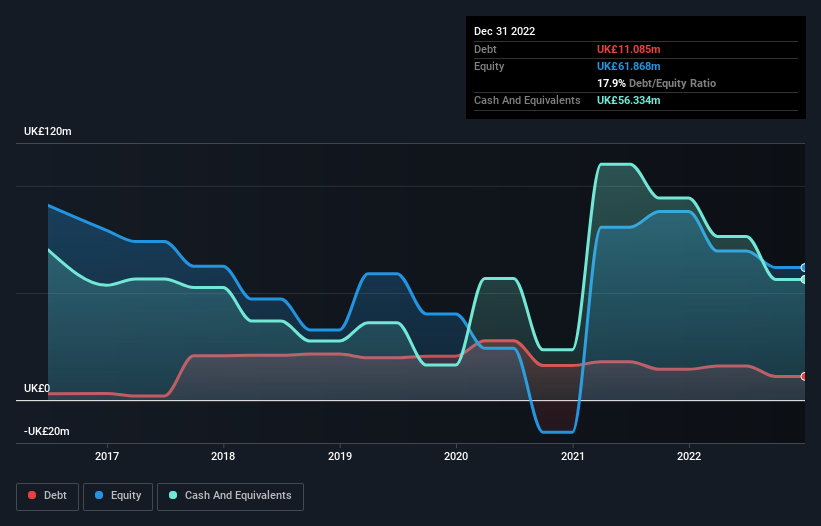

As you can see below, Mereo BioPharma Group had UK£11.1m of debt at December 2022, down from UK£14.4m a year prior. However, it does have UK£56.3m in cash offsetting this, leading to net cash of UK£45.2m.

How Strong Is Mereo BioPharma Group’s Balance Sheet?

We can see from the most recent balance sheet that Mereo BioPharma Group had liabilities of UK£24.7m falling due within a year, and liabilities of UK£1.53m due beyond that. On the other hand, it had cash of UK£56.3m and UK£2.38m worth of receivables due within a year. So it can boast UK£32.5m more liquid assets than total liabilities.

This surplus strongly suggests that Mereo BioPharma Group has a rock-solid balance sheet (and the debt is of no concern whatsoever). With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Succinctly put, Mereo BioPharma Group boasts net cash, so it’s fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Mereo BioPharma Group’s ability to maintain a healthy balance sheet going forward.

Since Mereo BioPharma Group doesn’t have significant operating revenue, shareholders may be hoping it comes up with a great new product, before it runs out of money.

So How Risky Is Mereo BioPharma Group?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Mereo BioPharma Group had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of UK£37m and booked a UK£34m accounting loss. Given it only has net cash of UK£45.2m, the company may need to raise more capital if it doesn’t reach break-even soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn’t produce free cash flow regularly.