Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies MercadoLibre, Inc. (NASDAQ:MELI) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is MercadoLibre’s Debt?

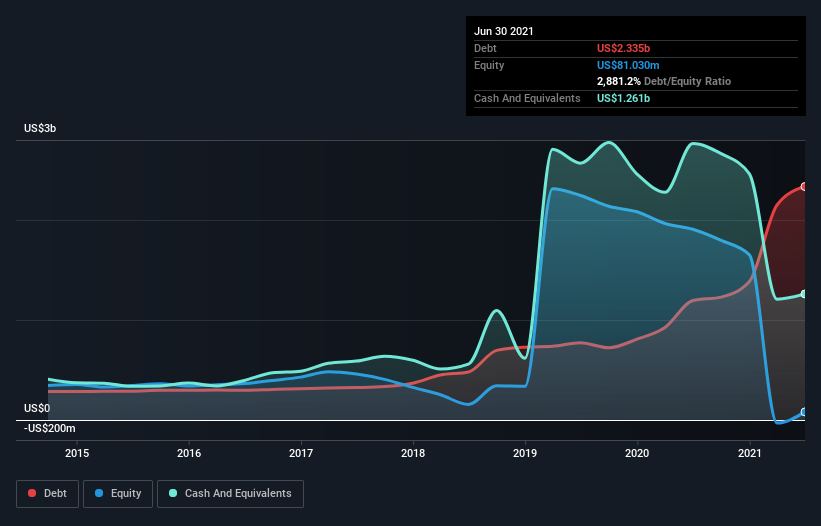

As you can see below, at the end of June 2021, MercadoLibre had US$2.33b of debt, up from US$1.19b a year ago. Click the image for more detail. However, it also had US$1.26b in cash, and so its net debt is US$1.07b.

How Strong Is MercadoLibre’s Balance Sheet?

The latest balance sheet data shows that MercadoLibre had liabilities of US$3.87b due within a year, and liabilities of US$2.19b falling due after that. Offsetting this, it had US$1.26b in cash and US$1.81b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.99b.

Given MercadoLibre has a humongous market capitalization of US$93.4b, it’s hard to believe these liabilities pose much threat. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. But either way, MercadoLibre has virtually no net debt, so it’s fair to say it does not have a heavy debt load!

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

We’d say that MercadoLibre’s moderate net debt to EBITDA ratio ( being 2.3), indicates prudence when it comes to debt. And its commanding EBIT of 13.4 times its interest expense, implies the debt load is as light as a peacock feather. We also note that MercadoLibre improved its EBIT from a last year’s loss to a positive US$322m. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if MercadoLibre can strengthen its balance sheet over time. So if you’re focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, MercadoLibre produced sturdy free cash flow equating to 57% of its EBIT, about what we’d expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

The good news is that MercadoLibre’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. And its conversion of EBIT to free cash flow is good too. All these things considered, it appears that MercadoLibre can comfortably handle its current debt levels. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet. There’s no doubt that we learn most about debt from the balance sheet.