David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Medtronic plc (NYSE:MDT) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

How Much Debt Does Medtronic Carry?

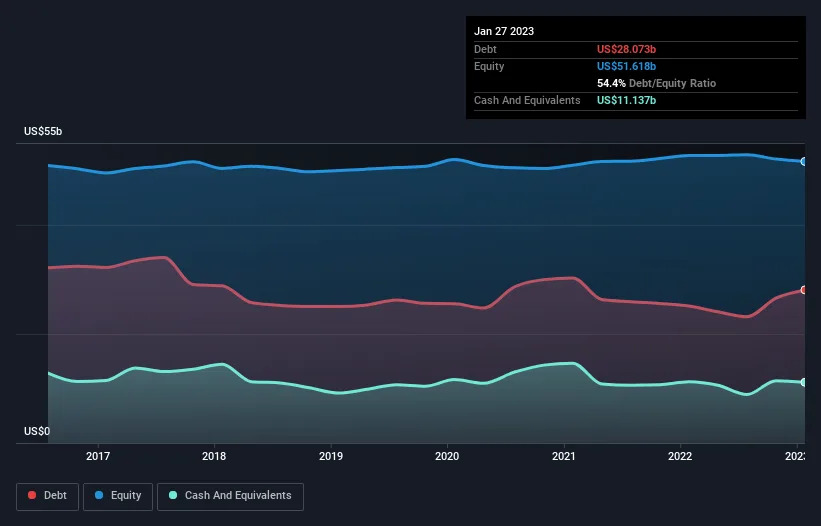

You can click the graphic below for the historical numbers, but it shows that as of January 2023 Medtronic had US$28.1b of debt, an increase on US$25.1b, over one year. However, because it has a cash reserve of US$11.1b, its net debt is less, at about US$16.9b.

A Look At Medtronic’s Liabilities

According to the last reported balance sheet, Medtronic had liabilities of US$14.4b due within 12 months, and liabilities of US$28.1b due beyond 12 months. On the other hand, it had cash of US$11.1b and US$5.89b worth of receivables due within a year. So its liabilities total US$25.5b more than the combination of its cash and short-term receivables.

Medtronic has a very large market capitalization of US$120.0b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

We’d say that Medtronic’s moderate net debt to EBITDA ratio ( being 2.0), indicates prudence when it comes to debt. And its strong interest cover of 12.3 times, makes us even more comfortable. Unfortunately, Medtronic’s EBIT flopped 15% over the last four quarters. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Medtronic can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Medtronic generated free cash flow amounting to a very robust 86% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

The good news is that Medtronic’s demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But we must concede we find its EBIT growth rate has the opposite effect. We would also note that Medical Equipment industry companies like Medtronic commonly do use debt without problems. All these things considered, it appears that Medtronic can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one.