Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. As with many other companies Magnite, Inc. (NASDAQ:MGNI) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

How Much Debt Does Magnite Carry?

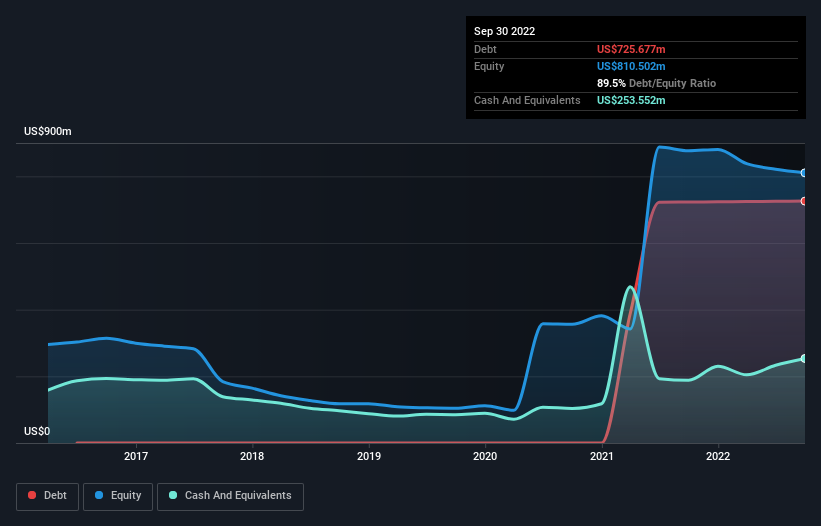

As you can see below, Magnite had US$725.7m of debt, at September 2022, which is about the same as the year before. You can click the chart for greater detail. However, it does have US$253.6m in cash offsetting this, leading to net debt of about US$472.1m.

How Healthy Is Magnite’s Balance Sheet?

According to the last reported balance sheet, Magnite had liabilities of US$919.0m due within 12 months, and liabilities of US$799.6m due beyond 12 months. On the other hand, it had cash of US$253.6m and US$804.4m worth of receivables due within a year. So its liabilities total US$660.7m more than the combination of its cash and short-term receivables.

Magnite has a market capitalization of US$1.44b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Magnite’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Magnite reported revenue of US$563m, which is a gain of 45%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

While we can certainly appreciate Magnite’s revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Indeed, it lost US$73m at the EBIT level. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. For example, we would not want to see a repeat of last year’s loss of US$93m. In the meantime, we consider the stock very risky. The balance sheet is clearly the area to focus on when you are analysing debt.