Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ So it seems the smart money knows that debt – which is usually involved in bankruptcies – is a very important factor, when you assess how risky a company is. We can see that Landstar System, Inc. (NASDAQ:LSTR) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

What Is Landstar System’s Debt?

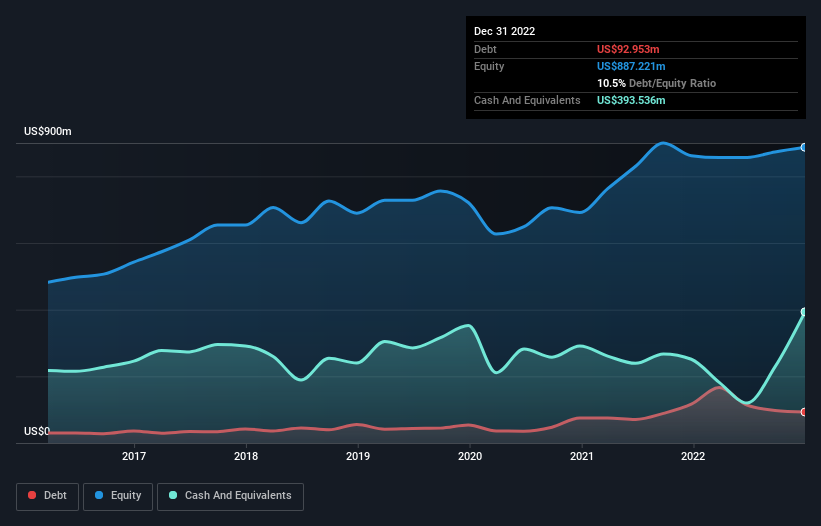

You can click the graphic below for the historical numbers, but it shows that Landstar System had US$93.0m of debt in December 2022, down from US$116.5m, one year before. However, it does have US$393.5m in cash offsetting this, leading to net cash of US$300.6m.

A Look At Landstar System’s Liabilities

Zooming in on the latest balance sheet data, we can see that Landstar System had liabilities of US$878.1m due within 12 months and liabilities of US$166.5m due beyond that. Offsetting this, it had US$393.5m in cash and US$1.02b in receivables that were due within 12 months. So it can boast US$372.9m more liquid assets than total liabilities.

This surplus suggests that Landstar System has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Landstar System boasts net cash, so it’s fair to say it does not have a heavy debt load!

And we also note warmly that Landstar System grew its EBIT by 12% last year, making its debt load easier to handle. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Landstar System’s ability to maintain a healthy balance sheet going forward.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Landstar System has net cash on its balance sheet, it’s still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, Landstar System recorded free cash flow worth 76% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Landstar System has net cash of US$300.6m, as well as more liquid assets than liabilities. The cherry on top was that in converted 76% of that EBIT to free cash flow, bringing in US$597m. So is Landstar System’s debt a risk? It doesn’t seem so to us. There’s no doubt that we learn most about debt from the balance sheet.