Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, JAKKS Pacific, Inc. (NASDAQ:JAKK) does carry debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is JAKKS Pacific’s Debt?

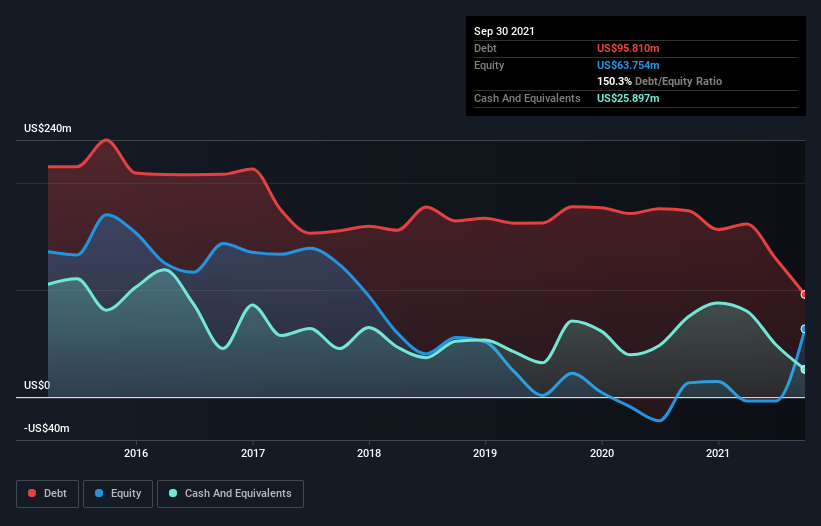

As you can see below, JAKKS Pacific had US$95.8m of debt at September 2021, down from US$173.9m a year prior. However, because it has a cash reserve of US$25.9m, its net debt is less, at about US$69.9m.

How Strong Is JAKKS Pacific’s Balance Sheet?

According to the last reported balance sheet, JAKKS Pacific had liabilities of US$224.1m due within 12 months, and liabilities of US$121.3m due beyond 12 months. Offsetting this, it had US$25.9m in cash and US$210.2m in receivables that were due within 12 months. So it has liabilities totalling US$109.3m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of US$122.2m. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While JAKKS Pacific has a quite reasonable net debt to EBITDA multiple of 1.5, its interest cover seems weak, at 2.1. This does have us wondering if the company pays high interest because it is considered risky. In any case, it’s safe to say the company has meaningful debt. Pleasingly, JAKKS Pacific is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 176% gain in the last twelve months. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if JAKKS Pacific can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last two years, JAKKS Pacific recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

To be frank both JAKKS Pacific’s interest cover and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Once we consider all the factors above, together, it seems to us that JAKKS Pacific’s debt is making it a bit risky. Some people like that sort of risk, but we’re mindful of the potential pitfalls, so we’d probably prefer it carry less debt. There’s no doubt that we learn most about debt from the balance sheet.