Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Jabil Inc. (NYSE:JBL) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Jabil Carry?

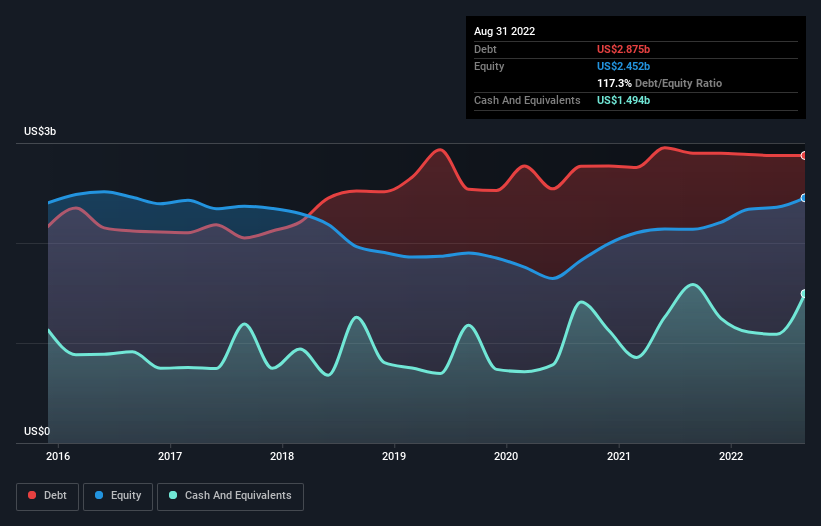

The chart below, which you can click on for greater detail, shows that Jabil had US$2.88b in debt in August 2022; about the same as the year before. On the flip side, it has US$1.49b in cash leading to net debt of about US$1.38b.

A Look At Jabil’s Liabilities

We can see from the most recent balance sheet that Jabil had liabilities of US$13.7b falling due within a year, and liabilities of US$3.57b due beyond that. Offsetting this, it had US$1.49b in cash and US$5.19b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$10.6b.

Given this deficit is actually higher than the company’s market capitalization of US$9.53b, we think shareholders really should watch Jabil’s debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 0.59 times EBITDA, Jabil is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 9.8 times the interest expense over the last year. In addition to that, we’re happy to report that Jabil has boosted its EBIT by 31%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Jabil can strengthen its balance sheet over time.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Jabil recorded free cash flow of 25% of its EBIT, which is weaker than we’d expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On our analysis Jabil’s EBIT growth rate should signal that it won’t have too much trouble with its debt. However, our other observations weren’t so heartening. In particular, level of total liabilities gives us cold feet. When we consider all the factors mentioned above, we do feel a bit cautious about Jabil’s use of debt. While we appreciate debt can enhance returns on equity, we’d suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt.