The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies International Seaways, Inc. (NYSE:INSW) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

What Is International Seaways’s Net Debt?

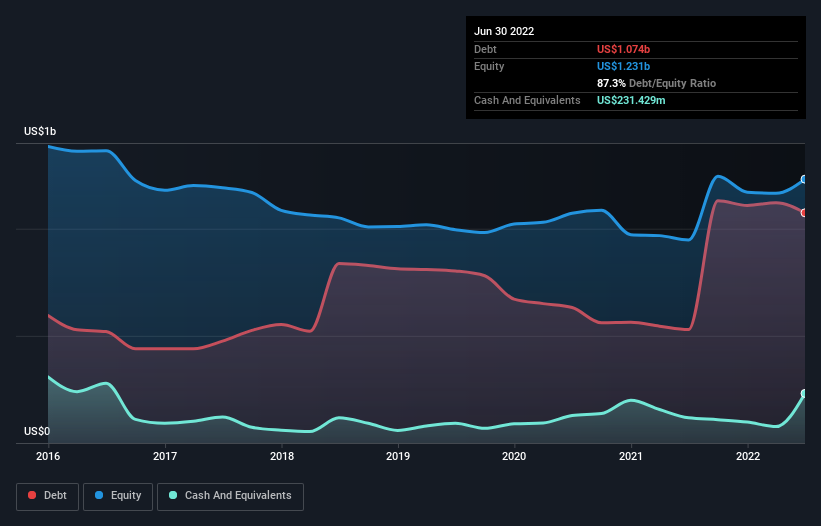

As you can see below, at the end of June 2022, International Seaways had US$1.07b of debt, up from US$529.3m a year ago. Click the image for more detail. On the flip side, it has US$231.4m in cash leading to net debt of about US$842.8m.

How Strong Is International Seaways’ Balance Sheet?

We can see from the most recent balance sheet that International Seaways had liabilities of US$208.9m falling due within a year, and liabilities of US$924.2m due beyond that. On the other hand, it had cash of US$231.4m and US$188.7m worth of receivables due within a year. So it has liabilities totalling US$713.0m more than its cash and near-term receivables, combined.

This deficit isn’t so bad because International Seaways is worth US$1.65b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it’s clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Weak interest cover of 0.58 times and a disturbingly high net debt to EBITDA ratio of 6.8 hit our confidence in International Seaways like a one-two punch to the gut. The debt burden here is substantial. One redeeming factor for International Seaways is that it turned last year’s EBIT loss into a gain of US$28m, over the last twelve months. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine International Seaways’s ability to maintain a healthy balance sheet going forward.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, International Seaways saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

To be frank both International Seaways’s interest cover and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But at least its EBIT growth rate is not so bad. Overall, it seems to us that International Seaways’s balance sheet is really quite a risk to the business. So we’re almost as wary of this stock as a hungry kitten is about falling into its owner’s fish pond: once bitten, twice shy, as they say.