David Iben put it well when he said, ‘Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that International Paper Company (NYSE:IP) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does International Paper Carry?

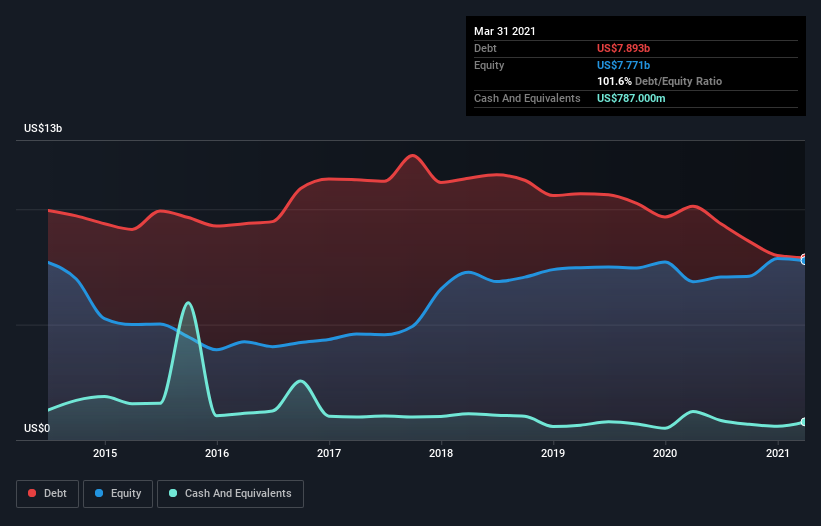

The image below, which you can click on for greater detail, shows that International Paper had debt of US$7.89b at the end of March 2021, a reduction from US$10.1b over a year. However, it also had US$787.0m in cash, and so its net debt is US$7.11b.

How Healthy Is International Paper’s Balance Sheet?

We can see from the most recent balance sheet that International Paper had liabilities of US$8.39b falling due within a year, and liabilities of US$15.3b due beyond that. On the other hand, it had cash of US$787.0m and US$3.78b worth of receivables due within a year. So it has liabilities totalling US$19.1b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its very significant market capitalization of US$23.6b, so it does suggest shareholders should keep an eye on International Paper’s use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

International Paper’s net debt is sitting at a very reasonable 2.4 times its EBITDA, while its EBIT covered its interest expense just 4.2 times last year. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. Shareholders should be aware that International Paper’s EBIT was down 23% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if International Paper can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of that EBIT is backed by free cash flow. Over the last three years, International Paper actually produced more free cash flow than EBIT. There’s nothing better than incoming cash when it comes to staying in your lenders’ good graces.

Our View

Neither International Paper’s ability to grow its EBIT nor its level of total liabilities gave us confidence in its ability to take on more debt. But the good news is it seems to be able to convert EBIT to free cash flow with ease. When we consider all the factors discussed, it seems to us that International Paper is taking some risks with its use of debt. So while that leverage does boost returns on equity, we wouldn’t really want to see it increase from here. There’s no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet.