Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Inotiv, Inc. (NASDAQ:NOTV) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

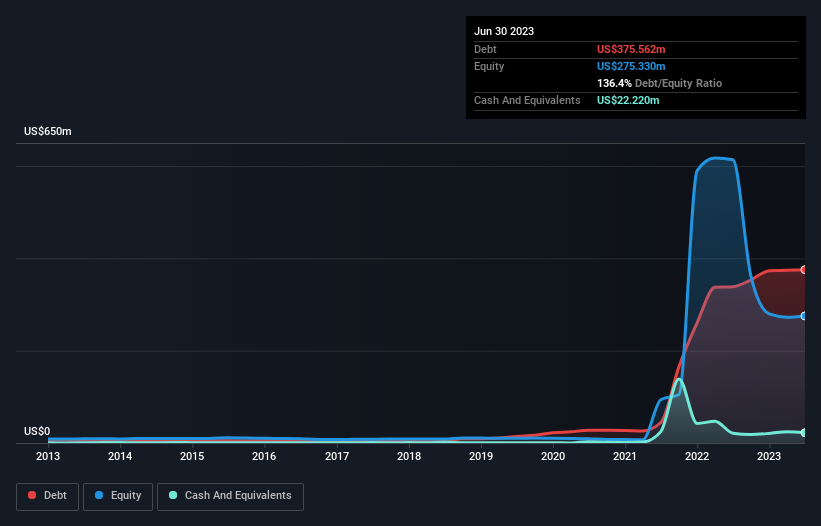

What Is Inotiv’s Net Debt?

The image below, which you can click on for greater detail, shows that at June 2023 Inotiv had debt of US$375.6m, up from US$338.8m in one year. However, it also had US$22.2m in cash, and so its net debt is US$353.3m.

How Strong Is Inotiv’s Balance Sheet?

The latest balance sheet data shows that Inotiv had liabilities of US$121.2m due within a year, and liabilities of US$458.3m falling due after that. On the other hand, it had cash of US$22.2m and US$84.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$472.6m.

This deficit casts a shadow over the US$50.3m company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. At the end of the day, Inotiv would probably need a major re-capitalization if its creditors were to demand repayment. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Inotiv can strengthen its balance sheet over time.

Over 12 months, Inotiv reported revenue of US$582m, which is a gain of 36%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Even though Inotiv managed to grow its top line quite deftly, the cold hard truth is that it is losing money on the EBIT line. Its EBIT loss was a whopping US$14m. Reflecting on this and the significant total liabilities, it’s hard to know what to say about the stock because of our intense dis-affinity for it. Like every long-shot we’re sure it has a glossy presentation outlining its blue-sky potential. But the reality is that it is low on liquid assets relative to liabilities, and it burned through US$17m in the last year. So is this a high risk stock? We think so, and we’d avoid it.