Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Illumina, Inc. (NASDAQ:ILMN) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Illumina’s Debt?

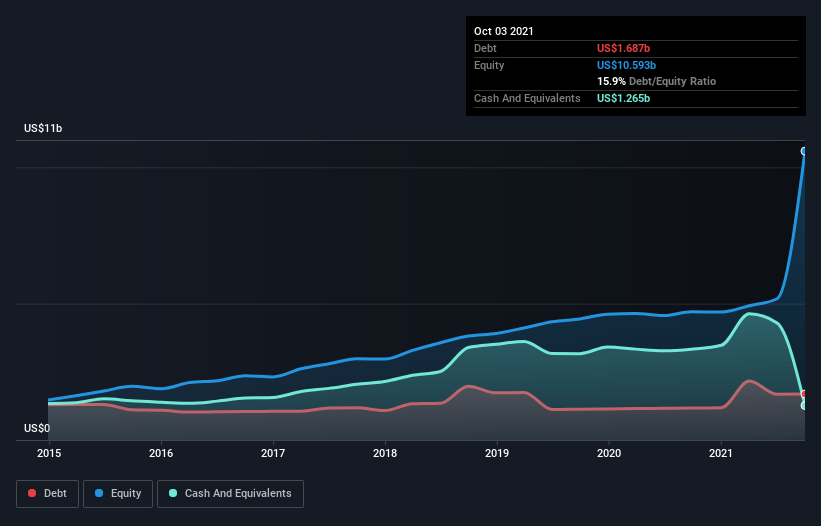

As you can see below, at the end of October 2021, Illumina had US$1.69b of debt, up from US$1.17b a year ago. Click the image for more detail. However, it does have US$1.27b in cash offsetting this, leading to net debt of about US$422.0m.

How Strong Is Illumina’s Balance Sheet?

According to the last reported balance sheet, Illumina had liabilities of US$914.0m due within 12 months, and liabilities of US$3.56b due beyond 12 months. Offsetting these obligations, it had cash of US$1.27b as well as receivables valued at US$604.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$2.60b.

Of course, Illumina has a titanic market capitalization of US$58.0b, so these liabilities are probably manageable. Having said that, it’s clear that we should continue to monitor its balance sheet, lest it change for the worse. But either way, Illumina has virtually no net debt, so it’s fair to say it does not have a heavy debt load!

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Illumina has a low net debt to EBITDA ratio of only 0.46. And its EBIT covers its interest expense a whopping 14.4 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. But the bad news is that Illumina has seen its EBIT plunge 16% in the last twelve months. If that rate of decline in earnings continues, the company could find itself in a tight spot. There’s no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Illumina’s ability to maintain a healthy balance sheet going forward.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Illumina generated free cash flow amounting to a very robust 85% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

Illumina’s interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14’s goalkeeper. But the stark truth is that we are concerned by its EBIT growth rate. Taking all this data into account, it seems to us that Illumina takes a pretty sensible approach to debt. While that brings some risk, it can also enhance returns for shareholders. There’s no doubt that we learn most about debt from the balance sheet.