The external fund manager backed by Berkshire Hathaway’s Charlie Munger, Li Lu, makes no bones about it when he says ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Hess Corporation (NYSE:HES) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

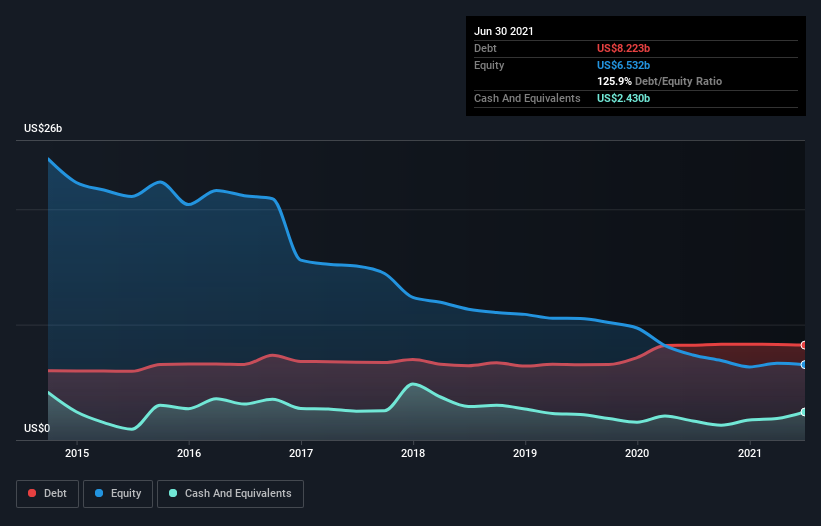

What Is Hess’s Debt?

The chart below, which you can click on for greater detail, shows that Hess had US$8.22b in debt in June 2021; about the same as the year before. However, it does have US$2.43b in cash offsetting this, leading to net debt of about US$5.79b.

A Look At Hess’ Liabilities

According to the last reported balance sheet, Hess had liabilities of US$2.53b due within 12 months, and liabilities of US$10.1b due beyond 12 months. On the other hand, it had cash of US$2.43b and US$1.00b worth of receivables due within a year. So it has liabilities totalling US$9.20b more than its cash and near-term receivables, combined.

While this might seem like a lot, it is not so bad since Hess has a huge market capitalization of US$22.0b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Hess has a quite reasonable net debt to EBITDA multiple of 2.0, its interest cover seems weak, at 2.0. The main reason for this is that it has such high depreciation and amortisation. These charges may be non-cash, so they could be excluded when it comes to paying down debt. But the accounting charges are there for a reason — some assets are seen to be losing value. In any case, it’s safe to say the company has meaningful debt. Notably, Hess made a loss at the EBIT level, last year, but improved that to positive EBIT of US$928m in the last twelve months. There’s no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Hess can strengthen its balance sheet over time.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Looking at the most recent year, Hess recorded free cash flow of 49% of its EBIT, which is weaker than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Hess’s interest cover was a real negative on this analysis, although the other factors we considered cast it in a significantly better light. But on the bright side, its ability to to convert EBIT to free cash flow isn’t too shabby at all. We think that Hess’s debt does make it a bit risky, after considering the aforementioned data points together. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. There’s no doubt that we learn most about debt from the balance sheet.