Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Hess Midstream LP (NYSE:HESM) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well – and to its own advantage. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Hess Midstream Carry?

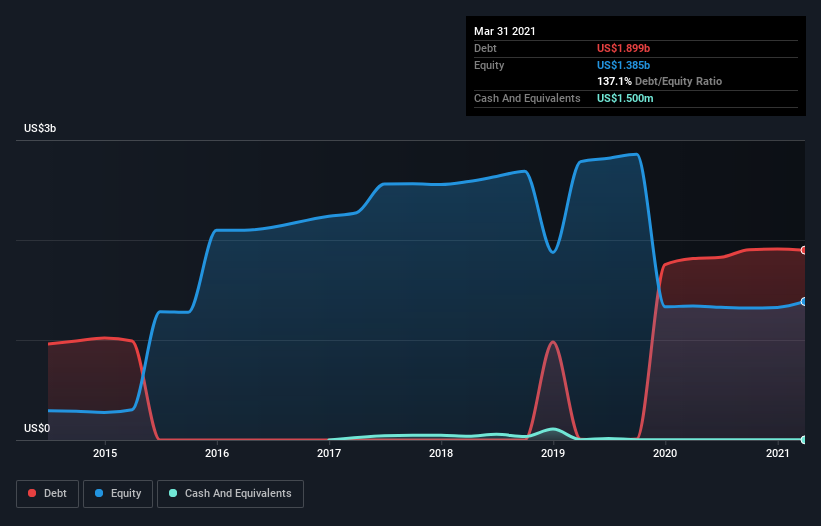

As you can see below, at the end of March 2021, Hess Midstream had US$1.90b of debt, up from US$1.81b a year ago. Click the image for more detail. Net debt is about the same, since the it doesn’t have much cash.

How Healthy Is Hess Midstream’s Balance Sheet?

We can see from the most recent balance sheet that Hess Midstream had liabilities of US$94.3m falling due within a year, and liabilities of US$1.91b due beyond that. On the other hand, it had cash of US$1.50m and US$108.1m worth of receivables due within a year. So its liabilities total US$1.89b more than the combination of its cash and short-term receivables.

Hess Midstream has a market capitalization of US$7.35b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Hess Midstream has net debt worth 2.5 times EBITDA, which isn’t too much, but its interest cover looks a bit on the low side, with EBIT at only 6.5 times the interest expense. While that doesn’t worry us too much, it does suggest the interest payments are somewhat of a burden. Importantly, Hess Midstream grew its EBIT by 32% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Hess Midstream can strengthen its balance sheet over time.

Finally, a business needs free cash flow to pay off debt; accounting profits just don’t cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Hess Midstream’s free cash flow amounted to 49% of its EBIT, less than we’d expect. That’s not great, when it comes to paying down debt.

Our View

Happily, Hess Midstream’s impressive EBIT growth rate implies it has the upper hand on its debt. But truth be told we feel its net debt to EBITDA does undermine this impression a bit. Looking at all the aforementioned factors together, it strikes us that Hess Midstream can handle its debt fairly comfortably. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it’s worth monitoring the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet – far from it.