Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Henry Schein, Inc. (NASDAQ:HSIC) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company’s use of debt, we first look at cash and debt together.

How Much Debt Does Henry Schein Carry?

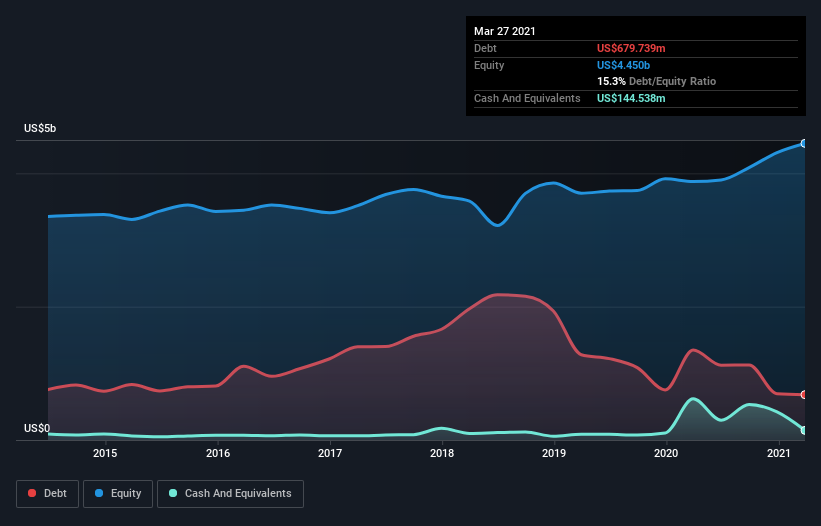

You can click the graphic below for the historical numbers, but it shows that Henry Schein had US$679.7m of debt in March 2021, down from US$1.35b, one year before. However, because it has a cash reserve of US$144.5m, its net debt is less, at about US$535.2m.

How Healthy Is Henry Schein’s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Henry Schein had liabilities of US$2.12b due within 12 months and liabilities of US$1.21b due beyond that. Offsetting this, it had US$144.5m in cash and US$1.32b in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.87b.

Given Henry Schein has a humongous market capitalization of US$11.2b, it’s hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We measure a company’s debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Henry Schein’s net debt is only 0.68 times its EBITDA. And its EBIT easily covers its interest expense, being 19.1 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. But the bad news is that Henry Schein has seen its EBIT plunge 18% in the last twelve months. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Henry Schein can strengthen its balance sheet over time.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of that EBIT is backed by free cash flow. During the last three years, Henry Schein generated free cash flow amounting to a very robust 92% of its EBIT, more than we’d expect. That puts it in a very strong position to pay down debt.

Our View

Happily, Henry Schein’s impressive interest cover implies it has the upper hand on its debt. But the stark truth is that we are concerned by its EBIT growth rate. It’s also worth noting that Henry Schein is in the Healthcare industry, which is often considered to be quite defensive. All these things considered, it appears that Henry Schein can comfortably handle its current debt levels. Of course, while this leverage can enhance returns on equity, it does bring more risk, so it’s worth keeping an eye on this one. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet.