Howard Marks put it nicely when he said that, rather than worrying about share price volatility, ‘The possibility of permanent loss is the risk I worry about… and every practical investor I know worries about.’ When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Health Catalyst, Inc. (NASDAQ:HCAT) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of ‘creative destruction’ where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company’s use of debt, we first look at cash and debt together.

What Is Health Catalyst’s Net Debt?

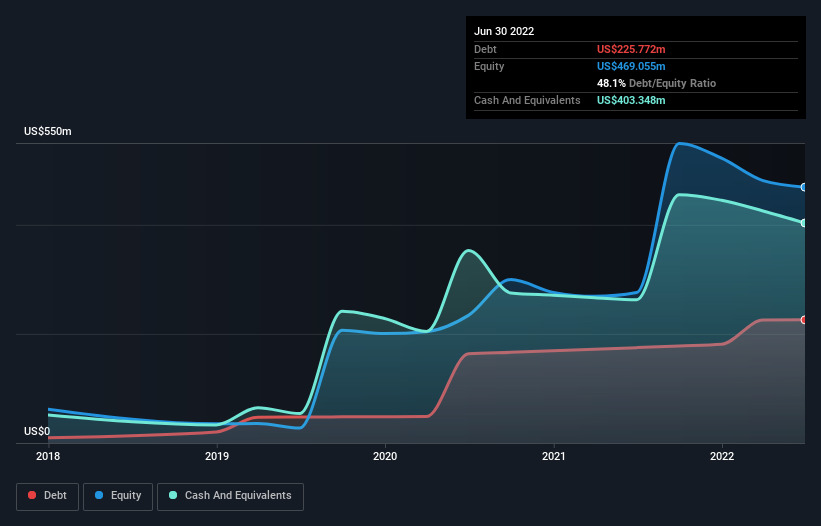

The image below, which you can click on for greater detail, shows that at June 2022 Health Catalyst had debt of US$225.8m, up from US$174.8m in one year. But on the other hand it also has US$403.3m in cash, leading to a US$177.6m net cash position.

How Healthy Is Health Catalyst’s Balance Sheet?

We can see from the most recent balance sheet that Health Catalyst had liabilities of US$90.3m falling due within a year, and liabilities of US$252.0m due beyond that. Offsetting these obligations, it had cash of US$403.3m as well as receivables valued at US$48.2m due within 12 months. So it can boast US$109.2m more liquid assets than total liabilities.

This surplus suggests that Health Catalyst is using debt in a way that is appears to be both safe and conservative. Given it has easily adequate short term liquidity, we don’t think it will have any issues with its lenders. Simply put, the fact that Health Catalyst has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Health Catalyst’s ability to maintain a healthy balance sheet going forward.

Over 12 months, Health Catalyst reported revenue of US$265m, which is a gain of 23%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Health Catalyst?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that Health Catalyst had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of US$40m and booked a US$145m accounting loss. While this does make the company a bit risky, it’s important to remember it has net cash of US$177.6m. That means it could keep spending at its current rate for more than two years. Health Catalyst’s revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course.