Warren Buffett famously said, ‘Volatility is far from synonymous with risk.’ It’s only natural to consider a company’s balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Haynes International, Inc. (NASDAQ:HAYN) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company’s debt levels is to consider its cash and debt together.

How Much Debt Does Haynes International Carry?

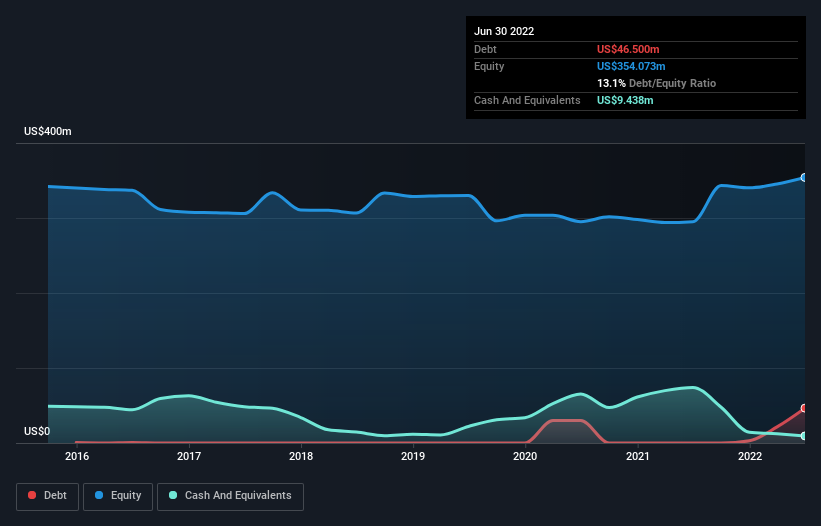

The image below, which you can click on for greater detail, shows that at June 2022 Haynes International had debt of US$46.5m, up from none in one year. On the flip side, it has US$9.44m in cash leading to net debt of about US$37.1m.

How Strong Is Haynes International’s Balance Sheet?

The latest balance sheet data shows that Haynes International had liabilities of US$138.6m due within a year, and liabilities of US$121.8m falling due after that. On the other hand, it had cash of US$9.44m and US$79.6m worth of receivables due within a year. So it has liabilities totalling US$171.4m more than its cash and near-term receivables, combined.

This deficit isn’t so bad because Haynes International is worth US$482.5m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company’s debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Haynes International’s net debt is only 0.58 times its EBITDA. And its EBIT covers its interest expense a whopping 24.2 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Although Haynes International made a loss at the EBIT level, last year, it was also good to see that it generated US$44m in EBIT over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Haynes International’s ability to maintain a healthy balance sheet going forward.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it’s worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. Over the last year, Haynes International saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

Neither Haynes International’s ability to convert EBIT to free cash flow nor its level of total liabilities gave us confidence in its ability to take on more debt. But its interest cover tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Haynes International is a somewhat risky investment as a result of its debt. That’s not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of.